1.0 NIGERIA’S FINANCIAL MARKET LANDSCAPE

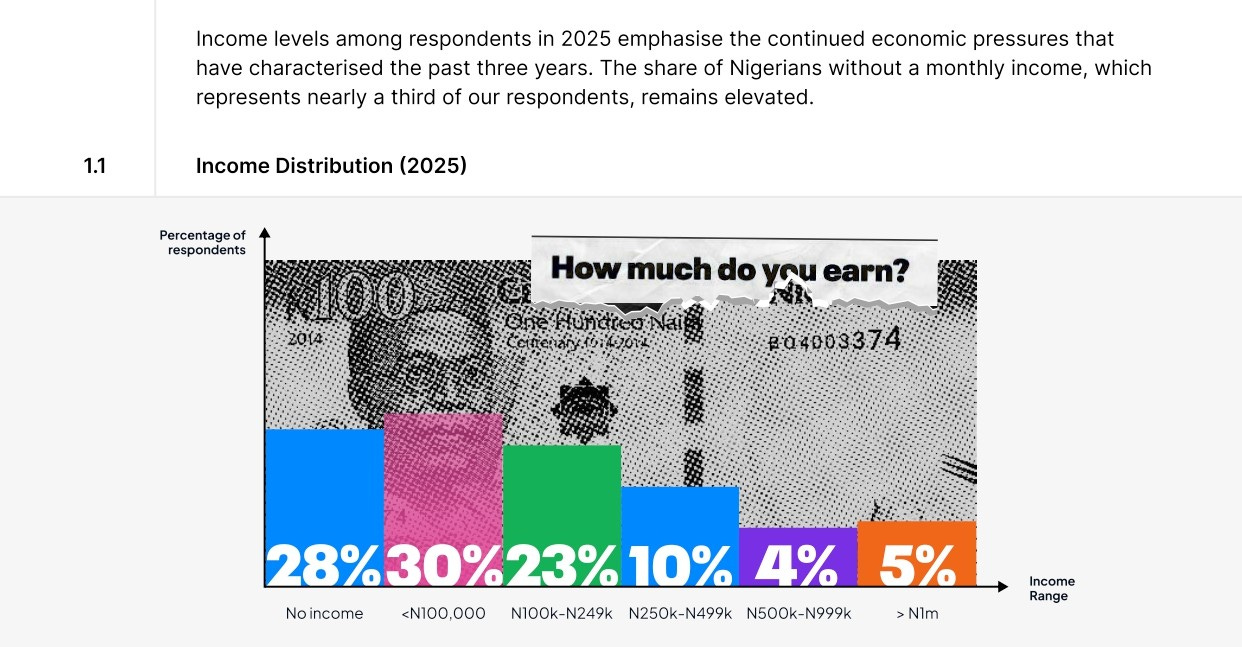

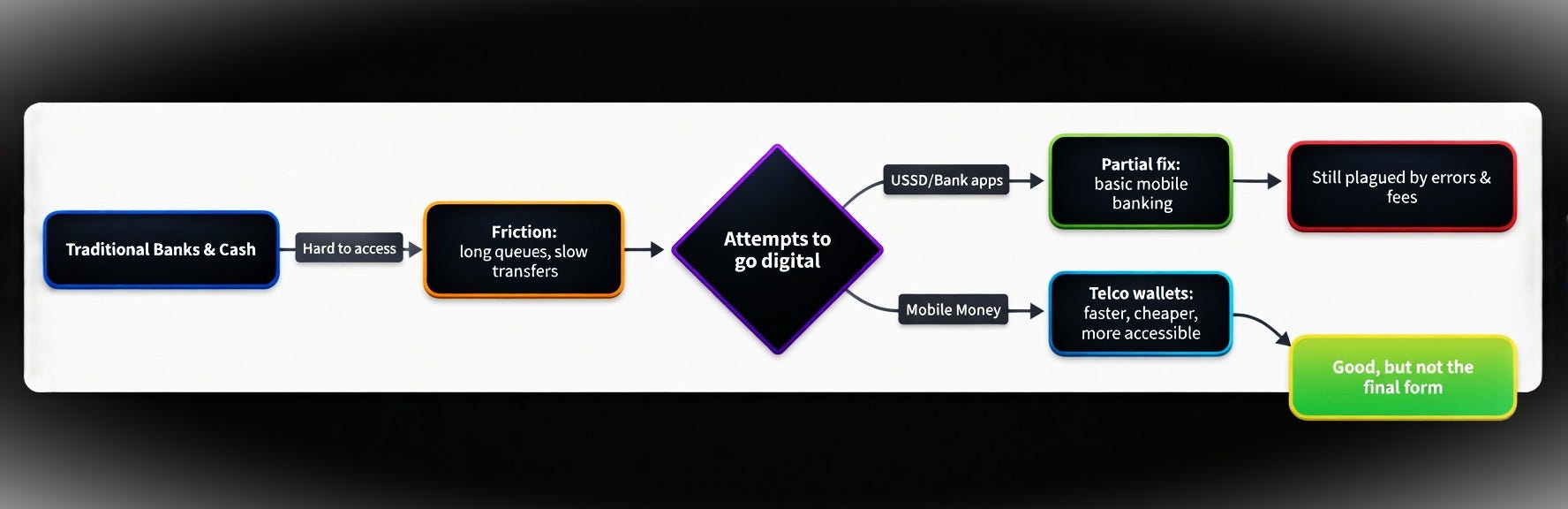

For a long time, the average Nigerian’s relationship with money has been, in many ways, bizarre and detached from reality. This disconnect is clearly captured in recent reports circulating in the media, reminding everyone of a ₦100,000 tax default levy, compounded by a ₦50,000 monthly increment,1 in a country where, as reported in March 2026 by PiggyVest, 30% of people earn less than ₦100,000 monthly and an additional 28% report no income at all.2

Somewhere along the line, the Nigerian financial system, and the authorities behind it, began expecting Nigerians to operate with the same financial strength and habits as people in far wealthier economies. Yet at the same time, they enforce a structure that sits far outside the earning reality of the average citizen, ignoring the country’s actual income levels and tax bracket.

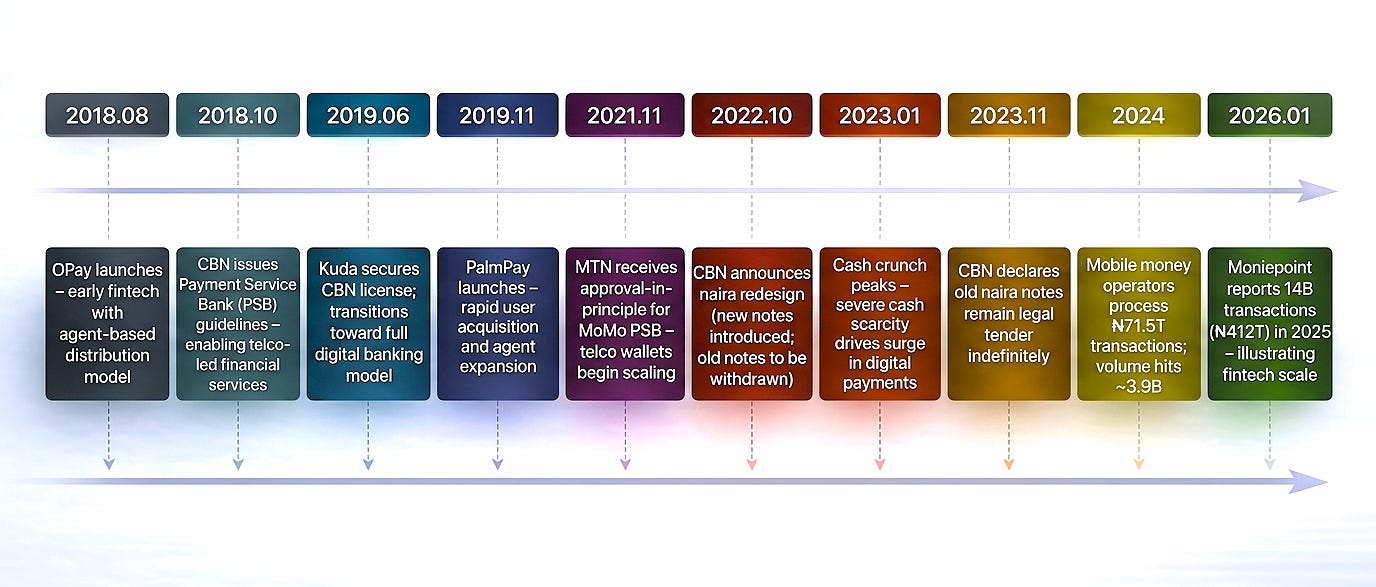

This bizarre relationship with money can be further illuminated by the cash scarcity that followed the Central Bank of Nigeria’s naira redesign policy. In October 2022, President Muhammadu Buhari backed the CBN’s decision to introduce new ₦200, ₦500 and ₦1,000 notes and withdraw the old ones from circulation.3 By January and February 2023, the country was gripped by severe cash shortages, forcing the CBN to extend deadlines,4 while protests broke out in several states as citizens struggled to access cash.5

While the Central Bank of Nigeria (CBN) initially withdrew over ₦1.3 trillion in old notes to curb hoarding and insecurity, it failed to inject sufficient new currency, resulting in a systemic collapse of the digital payment infrastructure and an estimated ₦20 trillion economic loss.6 This gap triggered a humanitarian crisis where citizens were forced to buy their own money from Point of Sale (POS) agents at interest rates exceeding 20%,7 an extortionate practice that has since evolved from a temporary shock into a permanent feature of the Nigerian economy.

The innovation of mobile banking, which is supposed to be liberation for Nigerians from the problems of traditional banking halls and chronic cash shortages, has instead proven that the apple truly doesn’t fall far from the tree. Reports have shown that as transaction volumes have skyrocketed, the infrastructure has buckled under the weight.

According to the Nigeria Inter-Bank Settlement System (NIBSS), electronic transactions surged to an staggering ₦600 trillion in 2023.8 The transaction value continued to rise into 2024, reaching an all-time high of approximately ₦1.07 quadrillion, representing nearly an 80 percent increase,9 and placing unprecedented pressure on digital systems that seem perpetually unready for the load. This strain shows up in everyday banking costs. For instance, despite the promise of lower overhead, excessive transaction charges remain deeply embedded in routine banking, from electronic transfer fees and SMS alert charges to card maintenance fees, all regulated under the CBN’s Guide to Charges by Banks.10

To add to that, when these systems fail, the resolution process is often as sluggish as a 1990s banking hall. The Federal Competition and Consumer Protection Commission (FCCPC) has repeatedly summoned banks over unresolved transfer failures and delayed refunds,11 and this trend has only intensified, with CBN data from 2025 showing a 143% spike in customer complaints, over half of which are tied specifically to electronic failures.12

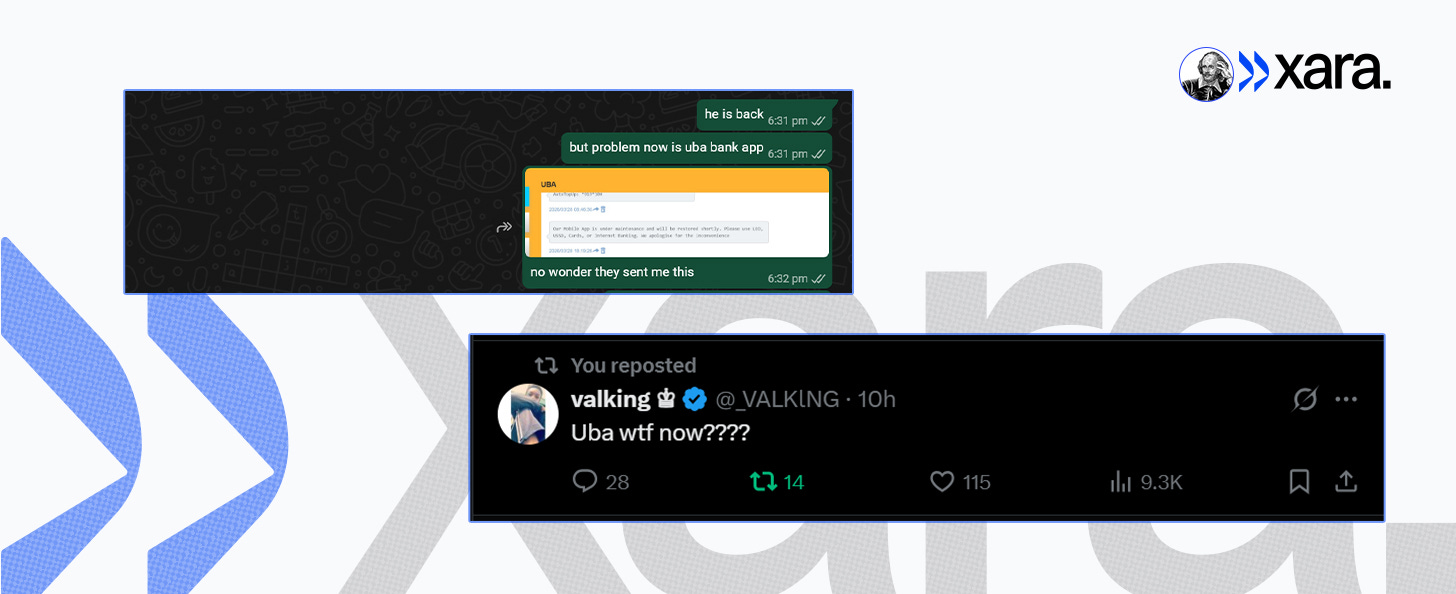

In a humorous yet frustrating twist, even i recently got caught in a banking app lockout where i couldn't access my funds or do anything with them, only to log onto X (formerly Twitter) many hours later to find a sea of complaints mirroring my exact issue.

It was a perfect, if painful, demonstration of why we cannot yet rely on these systems at scale. They have simply traded the physical queue for a digital one, and while the interface has changed, the underlying institutional deficit remains stubbornly intact.

2.0 ANATOMY OF THE SHIFT

Between 2022 and 2026, Nigeria experienced a seismic shift toward mobile money wallets, catalyzed by persistent gaps in traditional banking and the CBN’s aggressive cashless mandate. Leading the charge, licensed operators like OPay, PalmPay, Moniepoint, and Kuda processed ₦600 trillion in 2023, a 55% jump from the previous year.13 Momentum surged even further in 2024, with electronic payment volumes hitting an all-time high of ₦1.07 quadrillion (approx. $702 billion). This 80% increase in value, paired with a rise to 11.2 billion transactions,14 highlights a point of no return for digital adoption, with mobile wallets now firmly at the epicenter of daily commerce.

According to TechCabal, in 2025 Moniepoint alone processed ₦412 trillion in volume, which is nearly 40% of the entire country’s NIBSS volume from the previous year, 2024.15 The daily transactions on these platforms reached tens of millions, with OPay and PalmPay each processing well over 10 million transactions daily driven by their vast agent networks and retail dominance,16 Moniepoint handling millions of daily merchant-facing transactions across its POS infrastructure,17 and Kuda facilitating millions of app-based transfers daily within its growing digital banking ecosystem.18

But it wasn’t just persistent gaps in the banking sector and the Central Bank of Nigeria’s forced cashless push that drove this shift. Digital banking and bank apps existed before mobile money operators, so why are the latter winning in adoption and market penetration? I identify four core drivers:

High smartphone penetration

The shift to mobile money is directly tethered to the democratization of hardware. Driven by the availability of sub-$200 4G devices, smartphone shipments in Nigeria grew by roughly 25% in 2025.19 By the end of the year, active mobile connections reached roughly 165 million, representing about 69% penetration,20 while the number of smartphone users is projected to surpass 100 million by 2029.21 Brands like Transsion (Tecno/Infinix) and Samsung now hold over 50% of the market share,22 ensuring that even low-income earners have the hardware required to run apps like OPay or Moniepoint.

Easy onboarding and minimal KYC

Unlike traditional banks that historically required utility bills and physical presence, Mobile Money Operators utilized the Central Bank of Nigeria's Three-Tiered KYC framework to lower the barrier to entry.23 Formal financial inclusion rose from 57% in 2020 to 64% in 2023, fueled almost entirely by these non-bank services.24 Tier-1 accounts allow Nigerians to open a wallet with just a phone number, while biometric verification utilizing NIN or BVN allows for Tier-3 upgrades in a matter of minutes.

Fast, cheap, and transparent transactions

Mobile money operators offer near-perfect uptime and a near zero-fee structure. Their transaction success rates approach 99%, standing in stark contrast to the frequent system downtimes experienced with traditional commercial banks. Cost is also a key factor: Kuda provides up to 25 free interbank transfers each month,25 while PalmPay, OPay, and Moniepoint advertise unlimited free transfers alongside transfer success rates as high as 99.9%.26 Plus, these apps also make it easy to understand your spending habits by automatically organizing your transactions into clear categories such as utility bills, data, airtime, transfers, betting, etc.

Embedded features (loans, savings, etc.)

Mobile money apps have evolved into comprehensive super apps by moving far beyond simple transfers to offer high-yield savings and instant nano-loans based on transaction history rather than physical collateral. As of early 2026, Nigeria’s embedded finance market has reached a valuation of $4.34 billion, growing from a $3.99 billion baseline in 2024, and is now on track to expand to approximately $5.55 billion by 2030.27 To highlight this scale, Kuda issued over ₦16.4 billion in overdrafts in Q1 2025 alone,28 while Moniepoint disbursed over ₦1 trillion to small businesses, driving a 36% increase in business activity for borrowers.29 Mobile wallets now are basically complete wealth management tools for the unbanked.

So, Nigerians have been able to move their money around more easily and gain access to services that would have otherwise been impractical for the average person in traditional banking halls.

But what if we went further? What if money had more than just a balance—what if it had a voice? What if your money could talk… like, literally?

3.0 ARE TEXT-BASED FINANCIAL SERVICES VIABLE?

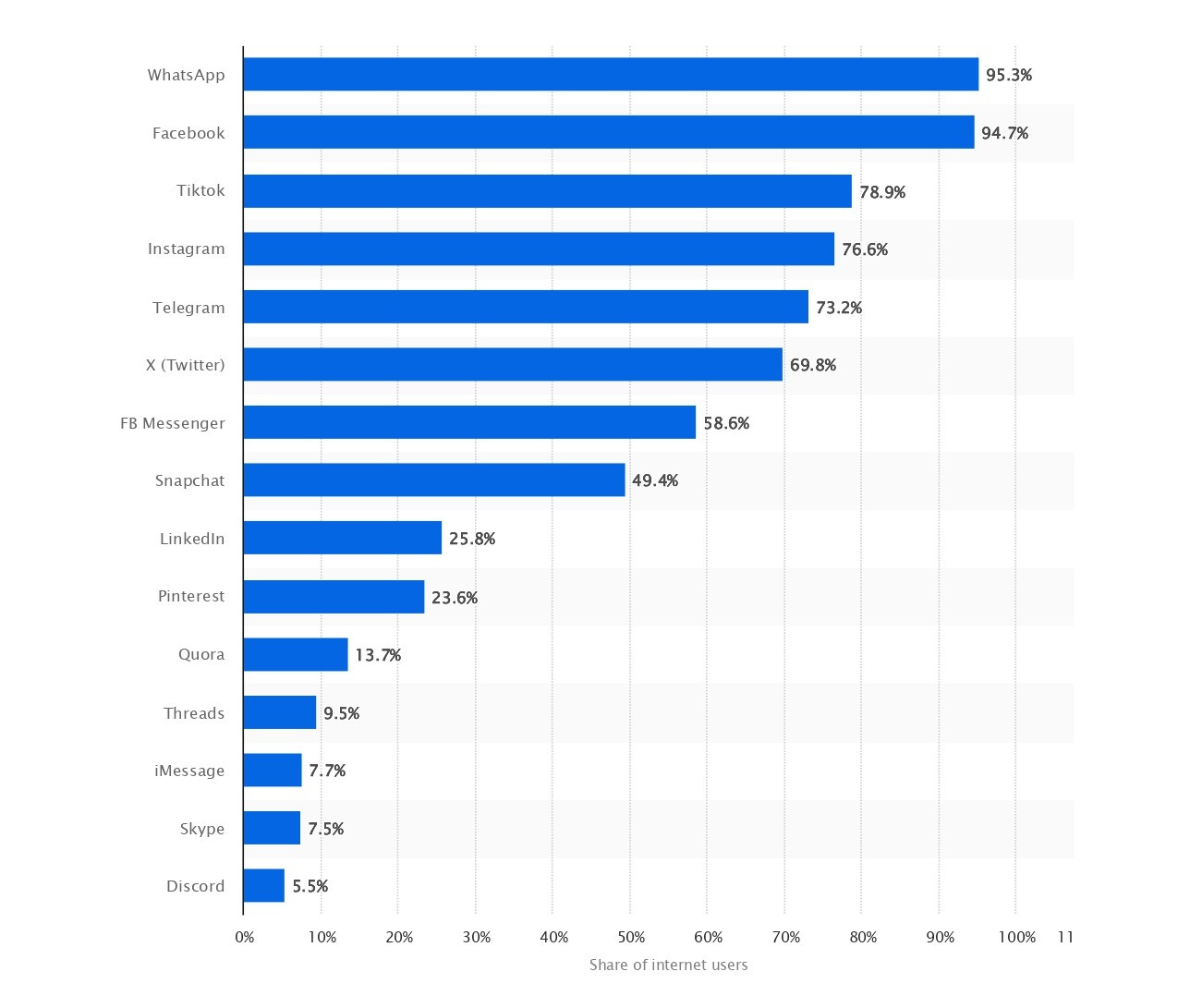

Messaging platforms sit at the center of social media’s rise and our growing dependence on phones and the internet. People already use text and voice-based interfaces to handle everyday tasks like communicating, sharing updates, receiving information, coordinating work, and moving through the day. Messaging is no longer just a feature of social media but has become an operating system for daily life. That familiarity is precisely what makes conversational financial services so compelling. Instead of asking people to learn a new banking app or download yet another wallet, financial services can be embedded into the same medium people already trust and use constantly.

In the global financial services landscape, there is an undergoing structural transformation that replaces traditional, menu-driven digital interfaces with fluid, intent-based natural language interactions. This evolution, commonly referred to as conversational banking, represents a fundamental move from reactive service models to proactive, agentic financial management. By bringing together artificial intelligence, large language models (LLMs), and ubiquitous messaging platforms, financial institutions are enabling users to manage and move money through text and voice commands that mirror human dialogue. 303132

The logic behind conversational banking is simple since it is essentially banking through voice or chat, where natural language tools interpret what the user wants, connect to account data, and guide them in real time. In practice, this can take the form of chatbots, WhatsApp banking, SMS banking, USSD menus, IVR systems, or voice assistants. The opportunity is bigger than convenience. It is distribution. It meets users where they already spend their time, and the marketing logic is clear as the customer acquisition cost (CAC) for services embedded in messaging apps can be as low as $0.02 to $0.50 per user, compared to $2 to $10 or more for standalone native apps.33

The global market for conversational AI in banking is projected to grow from $3.2 billion in 2025 to $7.8 billion by 2034, indicating significant industry recognition of LLMs' transformative potential.34

Conversational interfaces also address the inclusivity gap. Roughly 60% of banks worldwide currently fail to meet basic digital accessibility requirements.35 Natural Language Processing (NLP) models, provides an essential service for the elderly, the visually impaired, and individuals with limited digital literacy who struggle with physical or complex app interfaces.

By 2030, it is projected that 95% of customer interactions will be handled by AI chatbots as the default interface.36 This shift is driven by the efficiency of natural language, as a well-built AI can resolve up to 80% of routine inquiries instantly and significantly reduce the mental load and frustration associated with traditional IVR menus or long call center wait times. However, the channel must remain secure because SMS-based flows are exposed to risks like SIM-swap fraud, and even voice systems now face cloning threats, meaning the winning products will be those that combine convenience with stronger authentication and fraud controls.

In Nigeria, WhatsApp is the most used social media platform, which means a financial product embedded inside a familiar chat environment already has a stronger path to adoption than a standalone app users must go out of their way to install and learn. Nigerian financial institutions have pioneered this embedded approach to capture the active user base on WhatsApp and Facebook Messenger. For example, UBA’s Leo has already celebrated over 5.8 million users.37 And it is not even nearly as practical, efficient, or agentic as Xara.

4.0 ENTER XARA

Xara is an AI-powered, agentic financial assistant on WhatsApp that listens to your intent—via text, voice, or images—and simply makes it happen.

Whether you want to send money, pay bills, buy airtime or data for yourself or a friend, track your spending, gain insights into your financial habits, or even deposit and sell crypto for naira, all you have to do is ask Xara. It is an intuitive, proactive system that interprets and executes user intent for a negligible fee.

You wouldn’t be a beta tester either, as the app has already been live for over eight months, processed ₦8 billion in transaction volume,38 and scaled to 45,000 users over that period.39

As for how secure a WhatsApp-based banking interface is, Xara is certified by the Nigeria Data Protection Commission (NDPC), ensuring high standards of data protection and security in handling your financial data.

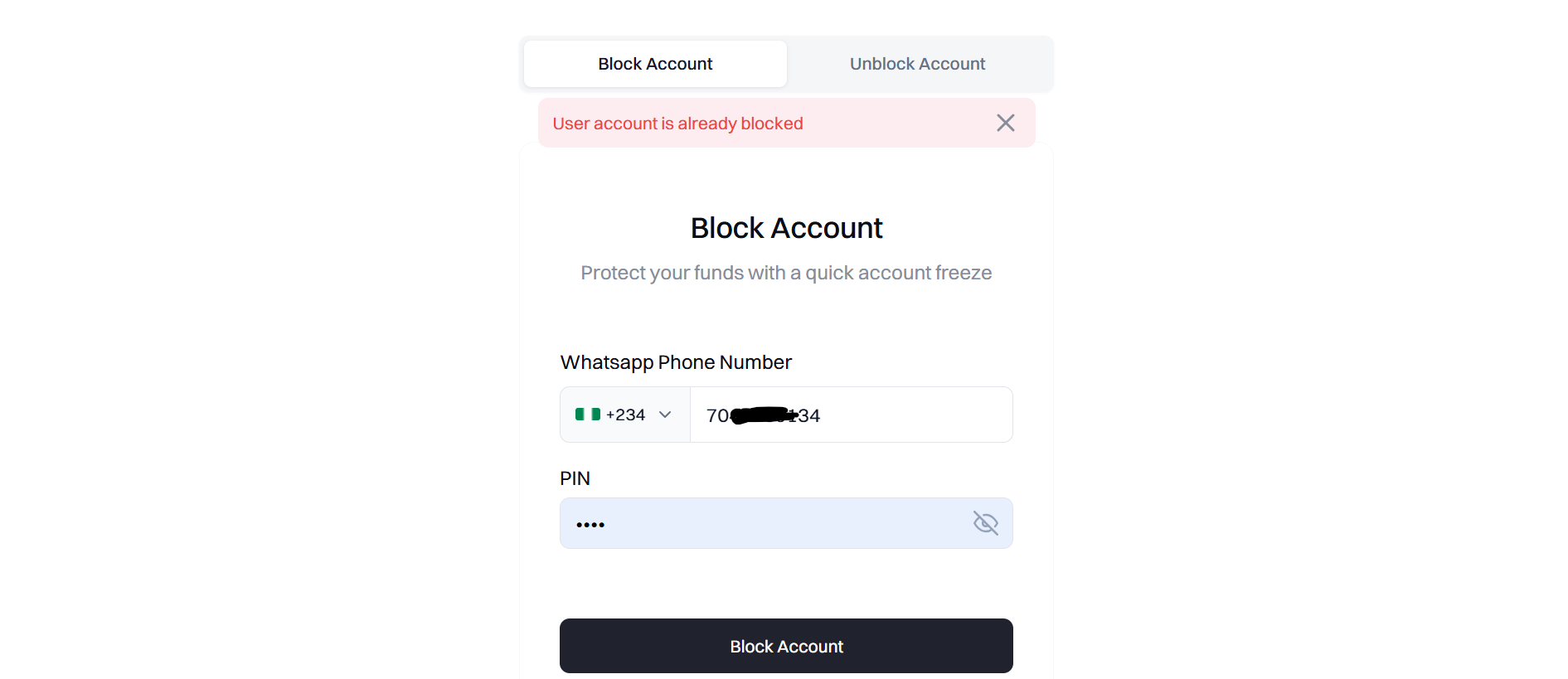

Every payment through Xara is protected by a PIN you create during setup, and you can set custom limits for when your passcode is required. Your Xara activity is also secured by your phone’s unlock system, and you can lock your individual conversations with Xara on WhatsApp as well.

In the event of a missing or stolen device, you can block your Xara account in seconds through the official website. This will freeze all payment activity until the account is unblocked.

4.1 SOLANA x XARA: TWO SIDES OF THE SAME COIN

Xara announced on the 25th of March 2026 that it has integrated Solana.40 This means users can now off-ramp their stablecoins on Solana through Xara. Upon deposit, Xara automatically converts USDC and USDT to naira, so you don’t even need to ask.

This isn’t just another marketing add-on or a superficial collaboration to hit KPIs. It is a deliberate design choice, as Solana is a crucial part of the Xara experience. While their roles are distinct, Xara as a product and Solana as a blockchain infrastructure, at their core they share the same vision, values, and philosophy. Both are enabling the fast, cheap, frictionless, and borderless movement of money.

Solana is the fastest and lowest-cost blockchain in production, and that performance has made it a natural fit for payment rails and stablecoin-based financial products both inside and outside crypto. On Solana, transactions are confirmed in less than a second (400ms) and cost a tiny fraction of a cent ($0.001). The network is designed to handle thousands of transactions every second (65,000 TPS) enabling high throughput at scale and making Solana suitable for real-world financial use.41 In fact, in 2025 alone, it processed over $1 trillion worth of stablecoin transactions.42

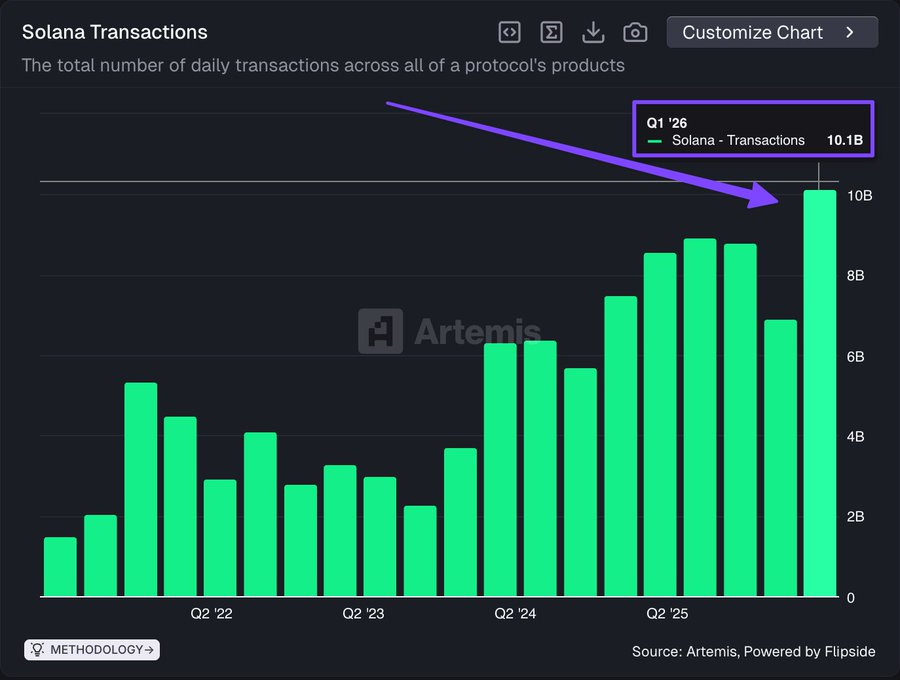

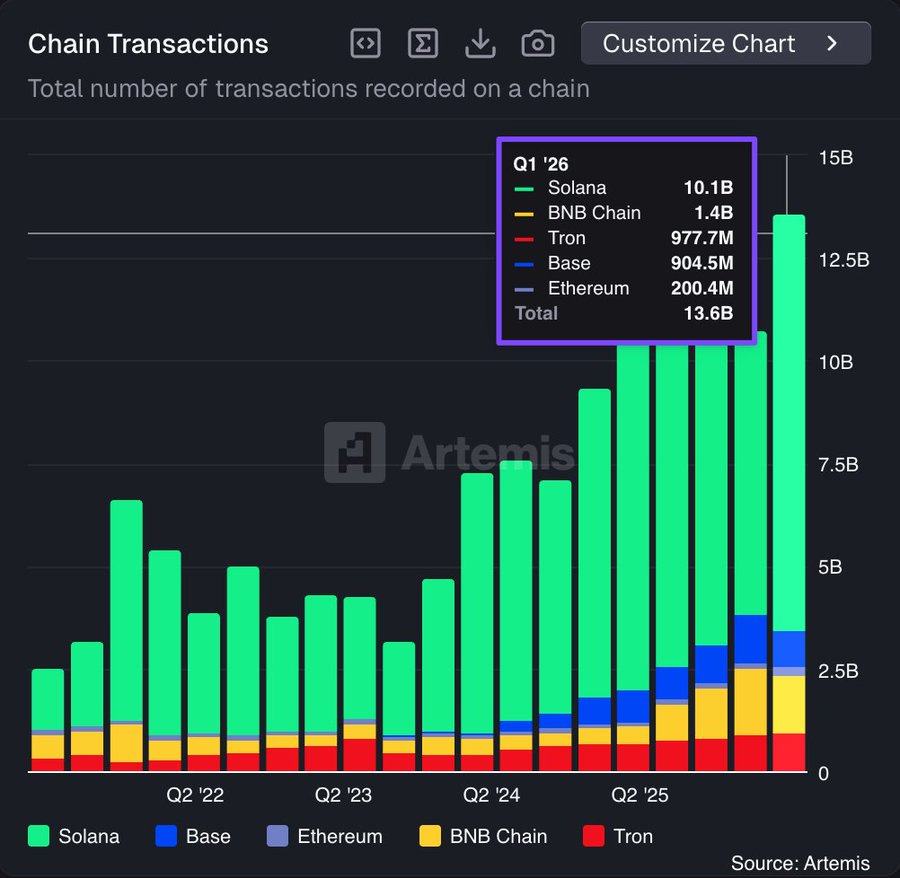

Artemis, a leading crypto analytics platform, reported that Solana surpassed 10 billion transactions in Q1 2026, marking a new all-time high.43 It is also important to note that this occurred during a “bear market.”

For context, even the nearest competitor, BNB Chain, recorded 8.7 billion fewer transactions than Solana over the same period.

If managing money starts with a text, then money should move like a text. Integrating Solana ensures that DeFi transactions on Xara are as instantaneous and affordable as sending a WhatsApp message. And that’s why Xara and Solana are two sides of the same coin.

4.2 INSIDE XARA: A VISUAL GUIDE

I’m tempted to skip this part of the article because you likely won’t need it.

You’re already familiar with the platform you’ll use to access Xara, which is WhatsApp. And Xara itself is highly intuitive and agentic; it can guide you as you use it. You can ask it anything, and if it’s a request that can be executed, it handles it for you. Still, for completeness, I’ll walk you through the basics, from setting up your account to funding it, sending money, buying airtime or data, paying a light bill, and finally off-ramping your Solana stablecoins. Best of all, I’ll perform some of these transactions using only text, others with voice alone, some in my native language (Igbo), and some using nothing but images. So, let’s see if Xara is truly up to it.

Beginning with the first step:

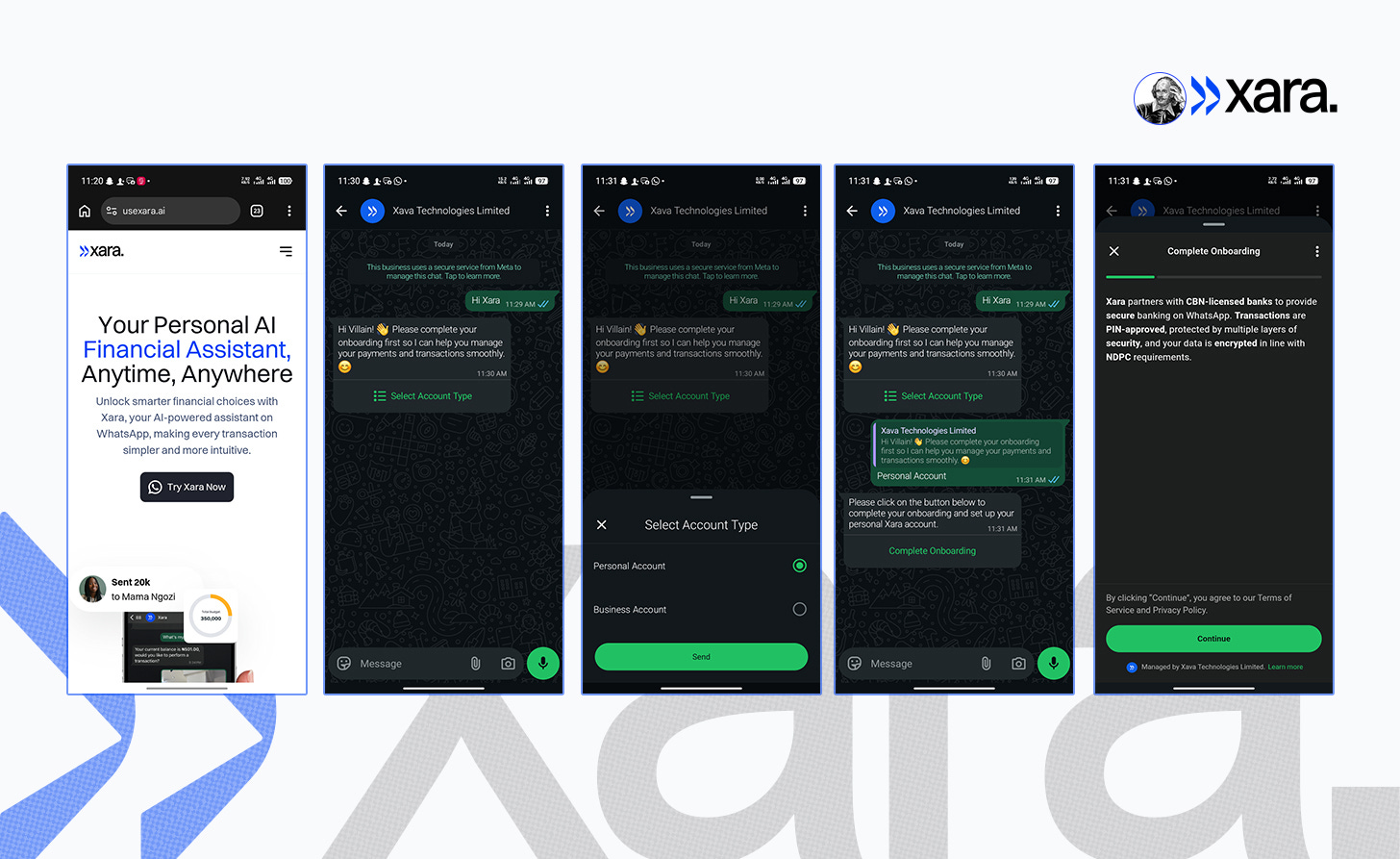

Step 1: Setting Up Your Xara Account

If you do not already have WhatsApp installed, this might be the sign you need to start using the app.

For iOS: WhatsApp on the App Store

For Android: WhatsApp on Google Play

After successfully installing and setting up your WhatsApp account, launch the Xara app by visiting their official website, or simply use the link below.

For iOS and Android: Launch usexara.ai

You’ll be required to select your account type after sending your first message to Xara. For this guide, I will be selecting the personal account option.

Note: Xara is built by Xava Technologies Limited, so the WhatsApp account appears as Xava Technologies Limited.

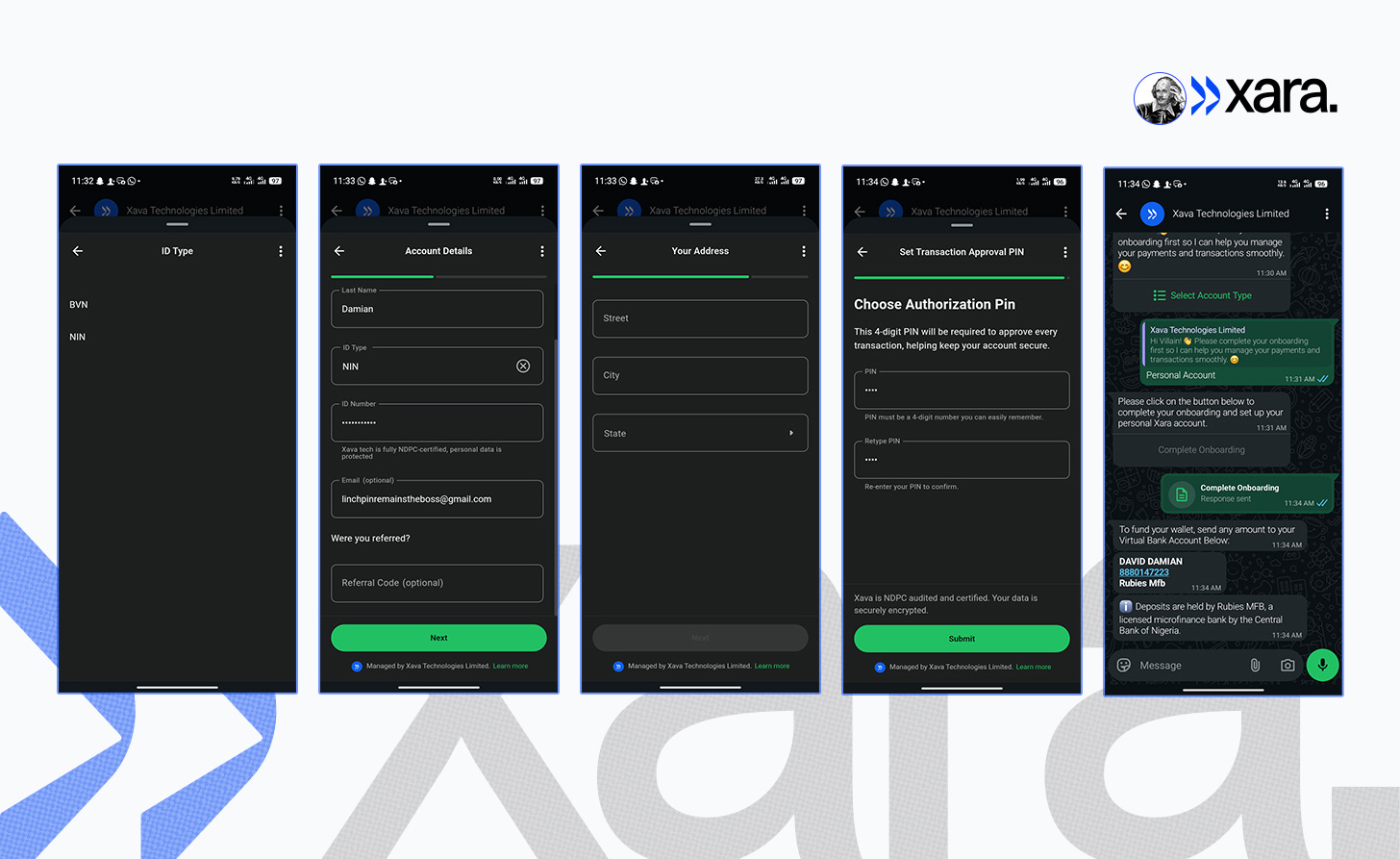

After that, proceed to complete onboarding by selecting your ID type from the two available options: National Identification Number (NIN) or Bank Verification Number (BVN).

Next, input your last name, the ID number corresponding to your selected ID, and optionally your email address, then click “Next.” You will need to provide your residential address on the following page, and after that, complete the final step, which is setting your authorization PIN. It is important to ensure that your PIN is not easily guessable.

Click “Submit,” and your onboarding will be complete. You’ll be returned to the main chat, where your virtual Xara bank name and account number will be available, ready for your first deposit.

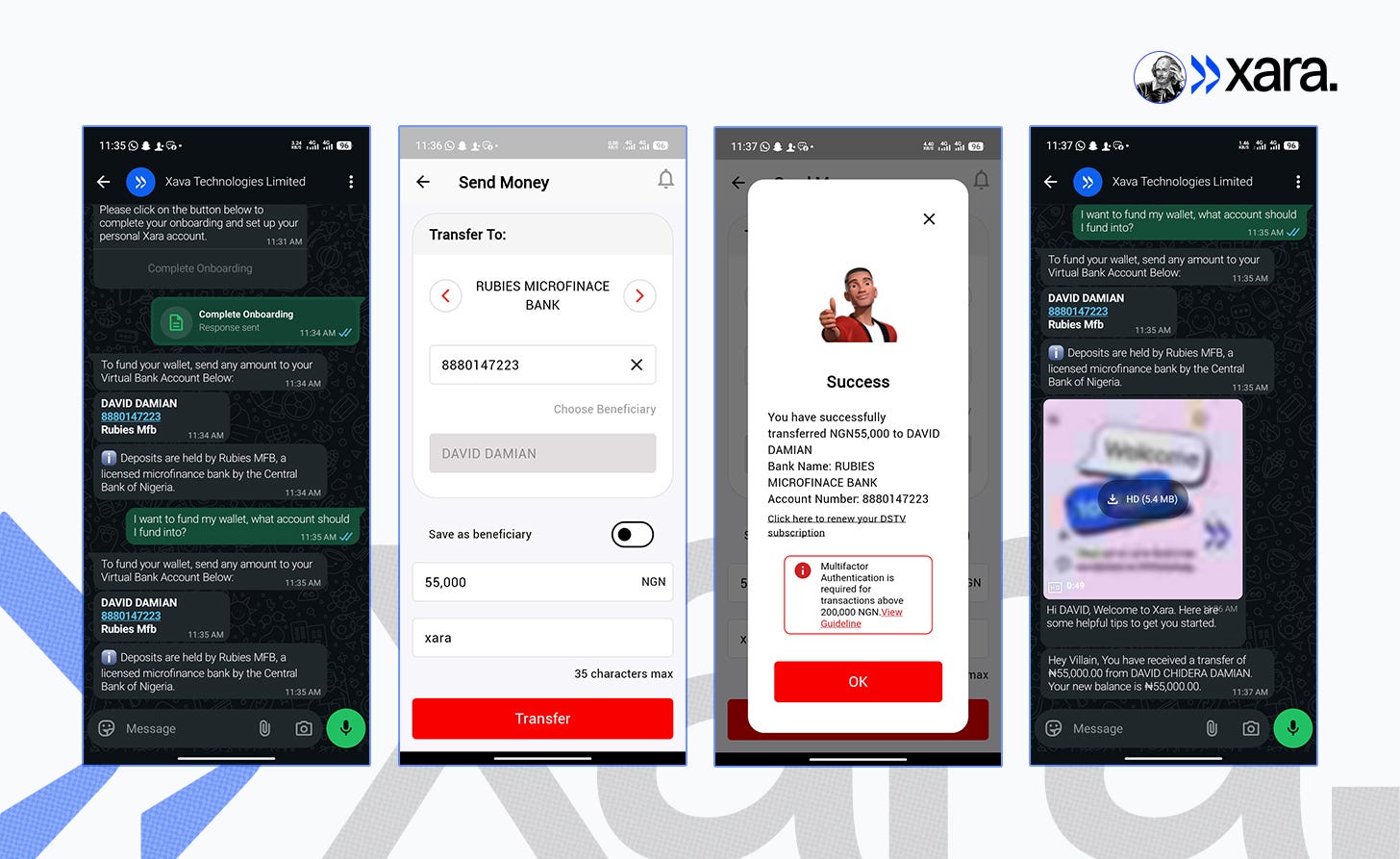

Step 2: Funding Your Xara Account

Simply copy the account number you’re given and send money to it via transfer. Xara confirms the deposit and updates your balance in seconds. For example, you can see I made my transfer at 11:37 AM, and Xara confirmed the deposit within that same minute. Now let’s actually put Xara to work.

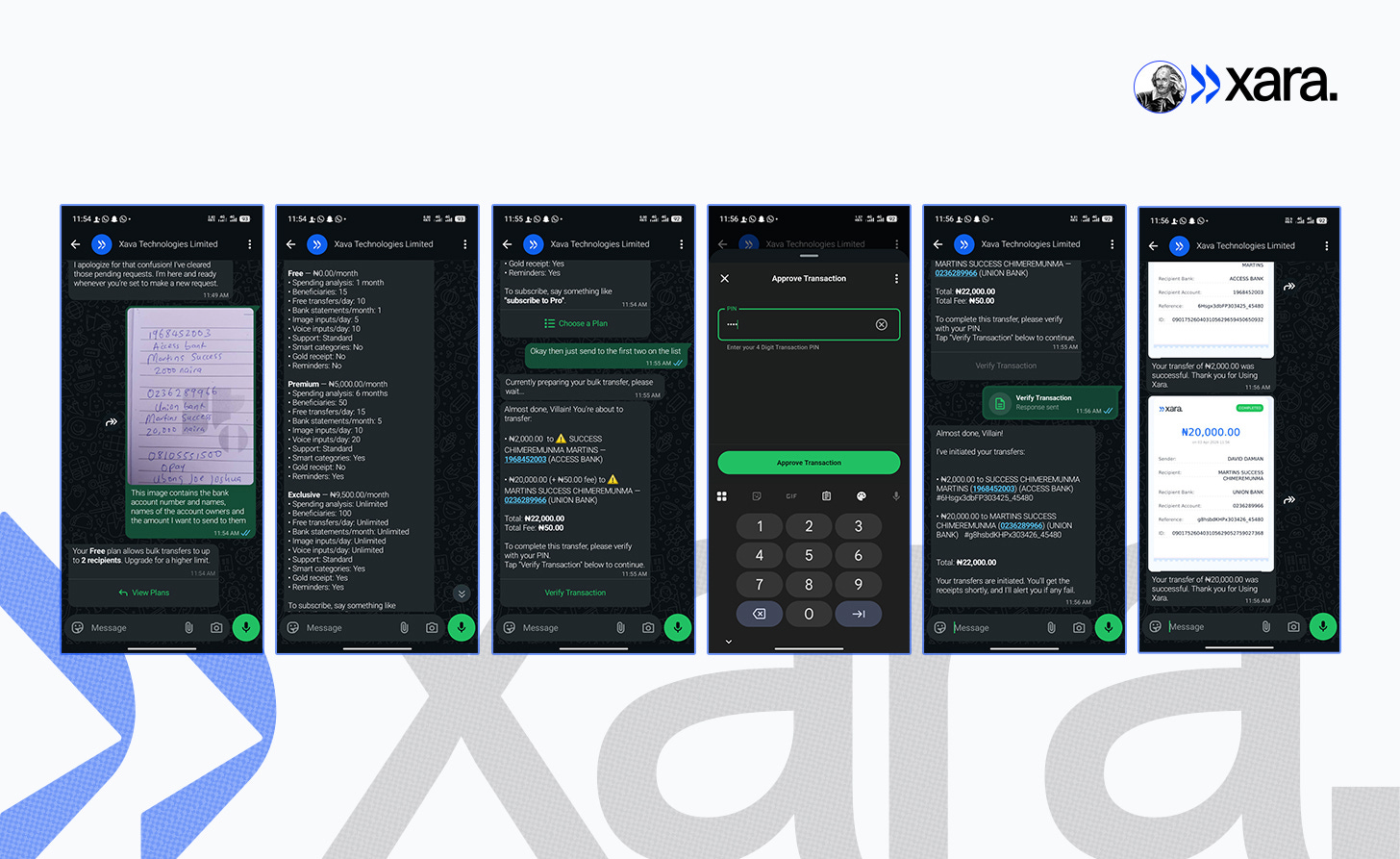

Test 1: Sending Bulk Transfers via Image Recognition

Note: A ₦50 Electronic Money Transfer Levy (EMTL) applies to all electronic transfers of ₦10,000 and above. This is a federal levy mandated by the Finance Act and the CBN.44 So, the ₦50 fee Xara displays on transfers above ₦10,000 is not their own charge, but a mandated levy. Xara offers three free transfers on the free tier; after that, a ₦10 service fee is applied to subsequent transfers.

To push Xara’s capabilities, I skipped the easy route of using a single account number. Instead, I wrote down three different account names, numbers, and amounts on a piece of paper. I then took a photo and uploaded it to the chat.

It was at this point that i discovered that I was on the Free Tier, which limits bulk transfers to two recipients per transaction. However, after instructing Xara to proceed with the first two transfers, it generated a verification prompt in seconds. Once I authorized it, both transactions were executed in under a minute.

Verdict: Even with tier-based limits, Xara’s OCR (Optical Character Recognition) is remarkably accurate and fast.

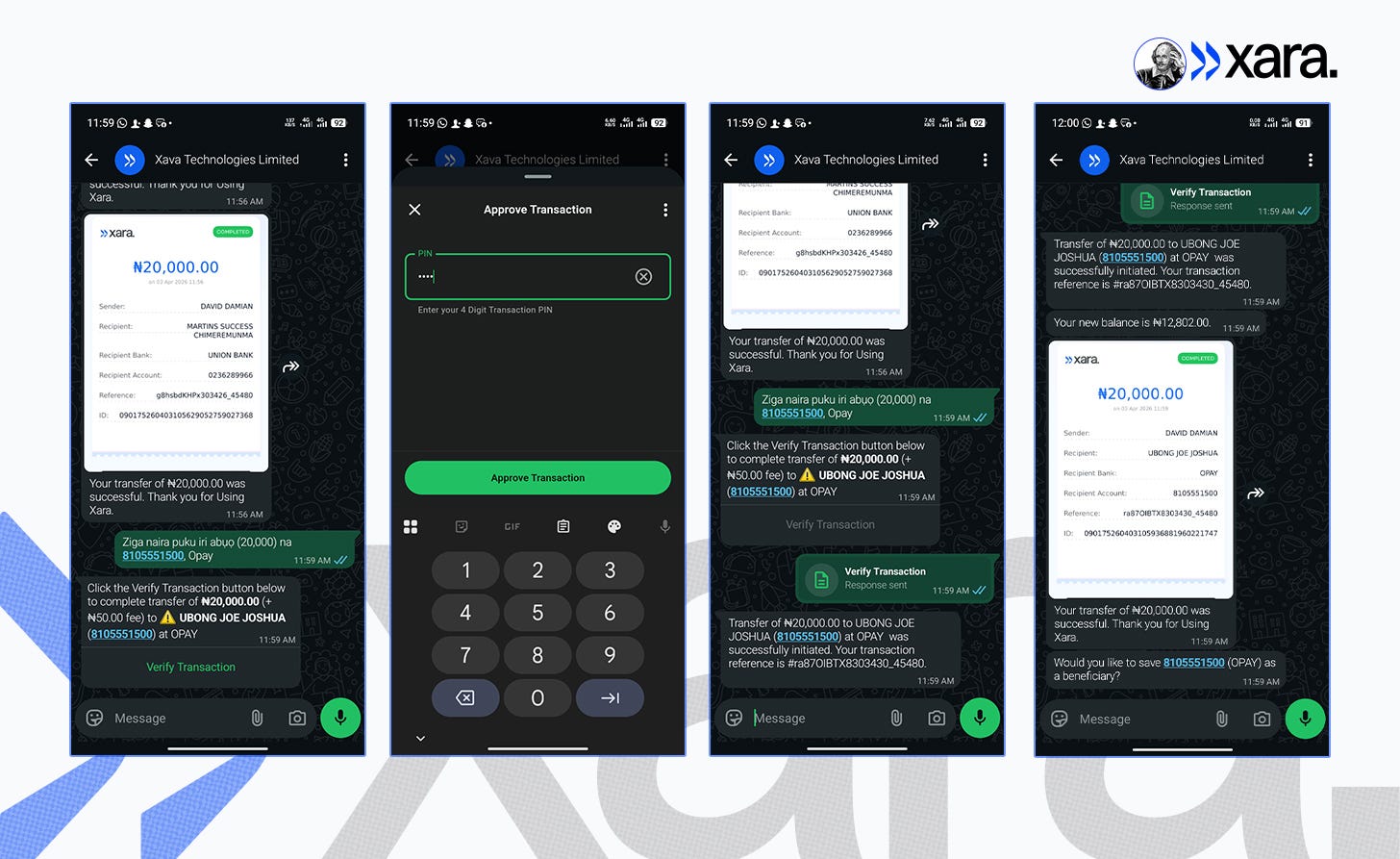

Test 2: Completing the Third Transfer Using My Native Language (Igbo)

I decided to complete the third transfer using Igbo, to see if Xara could handle a request in my native language. I sent the message: “Ziga naira puku iri abuo (20,000) na 8105551500. Opay,” which translates to “Send twenty thousand Naira (₦20,000) to 8105551500 on Opay.”

By this point, I shouldn’t have been surprised, but it was still impressive. Xara immediately recognized the instruction and prompted me to verify the transaction. After I confirmed, the transfer was initiated and completed, all in under a minute.

Verdict: Xara’s multilingual support is seamless, making banking accessible in the language you’re most comfortable with.

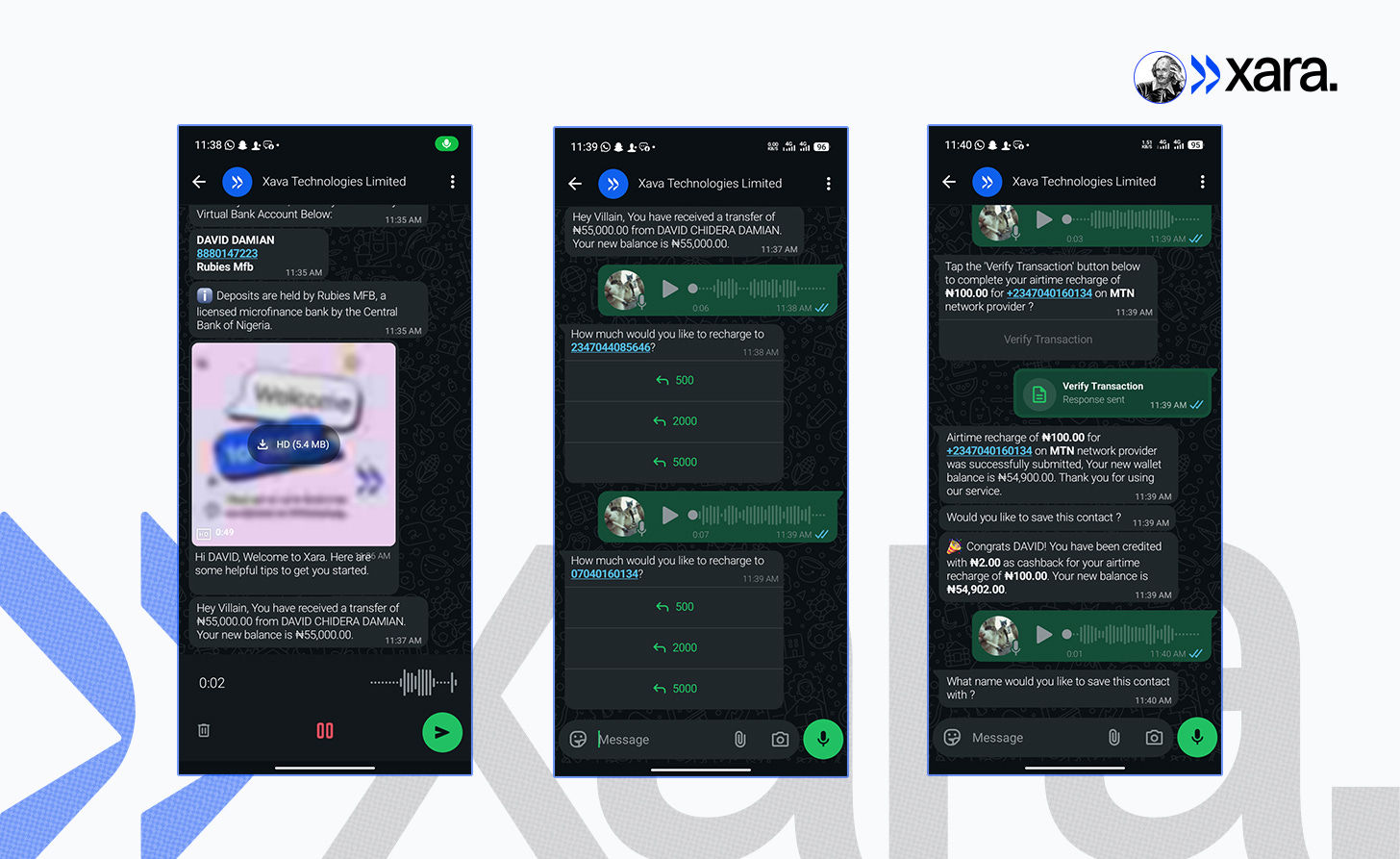

Test 3: Purchasing Airtime via Voice Instructions

Fun Fact: Xara users have topped up a staggering ₦30 million in airtime45 and loaded over 6,000gb of data!46

I tested Xara’s voice note functionality by recording a request to buy airtime. Xara responded promptly, asking for the recharge amount for my registered number and providing quick-tap options like 500, 2000, and 5000.

To test its precision, I sent another voice note specifying a different phone number. Xara correctly identified the new number and asked for the amount again. I replied via voice note requesting a recharge of only 100 Naira; Xara prompted me to verify the transaction, and the airtime was delivered instantly, along with a 2 Naira cashback.

Verdict: Xara passed the voice instruction test with flying colors.

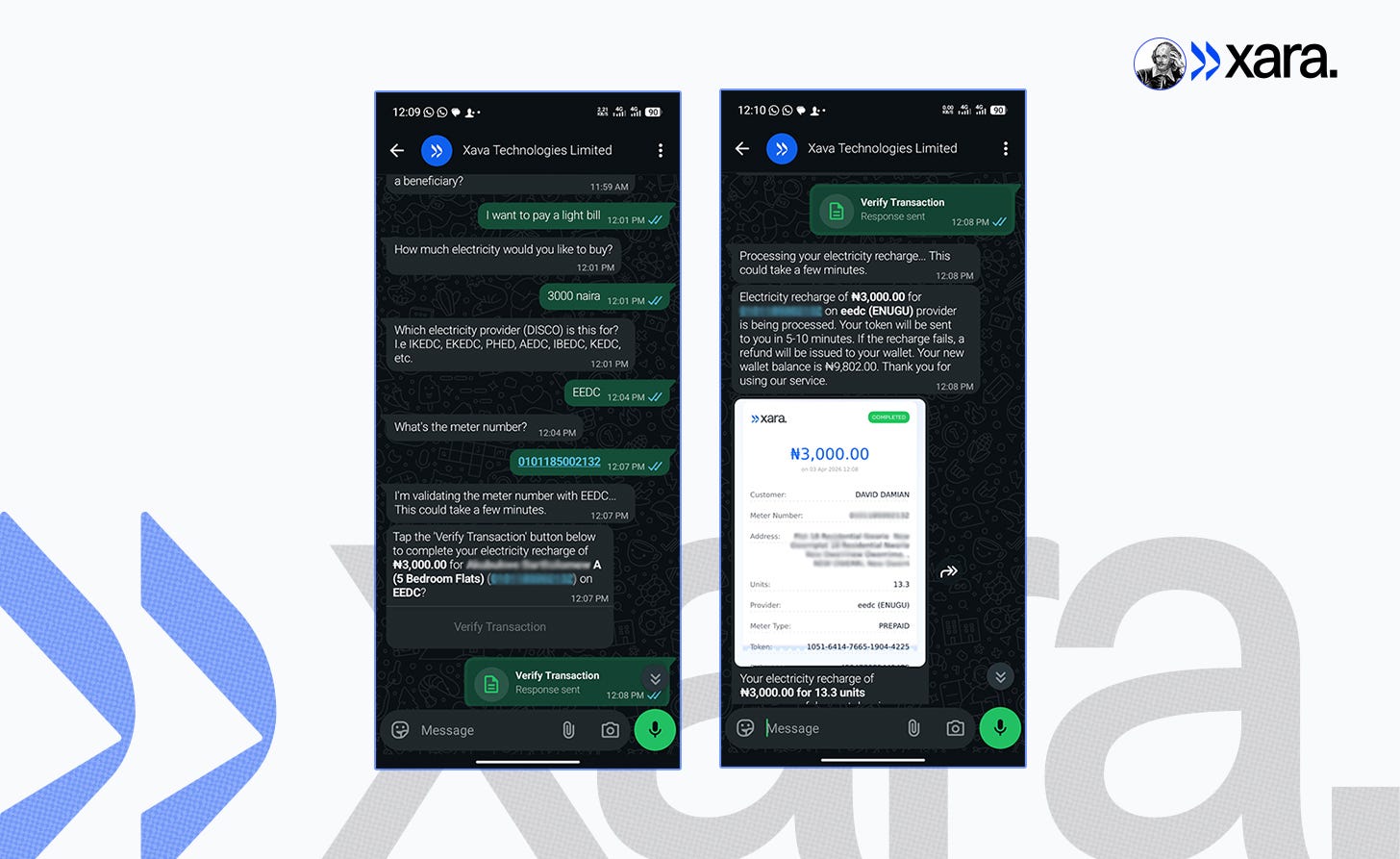

Test 4: Paying a Utility Bill (Electricity)

For my next test, I decided to pay my electricity bill. Full disclosure: I had never paid a light bill before, so I was completely oblivious to the process. I simply texted Xara my intent, and it responded by asking how much electricity I wanted to purchase. I requested ₦3,000 worth.

Xara then asked for the electricity provider. Since I didn’t know, I called my cousin, who told me it was “EEDC.” After I provided the provider’s name, Xara requested the meter number. Another quick call to my cousin got me the digits, which I passed along to the chat.

Xara immediately validated the meter number with EEDC and prompted me to verify the transaction. Once confirmed, the payment was processed, and Xara sent me the token number to complete the recharge.

Verdict: Xara makes complex utility payments feel like a simple conversation, even for a first-timer.

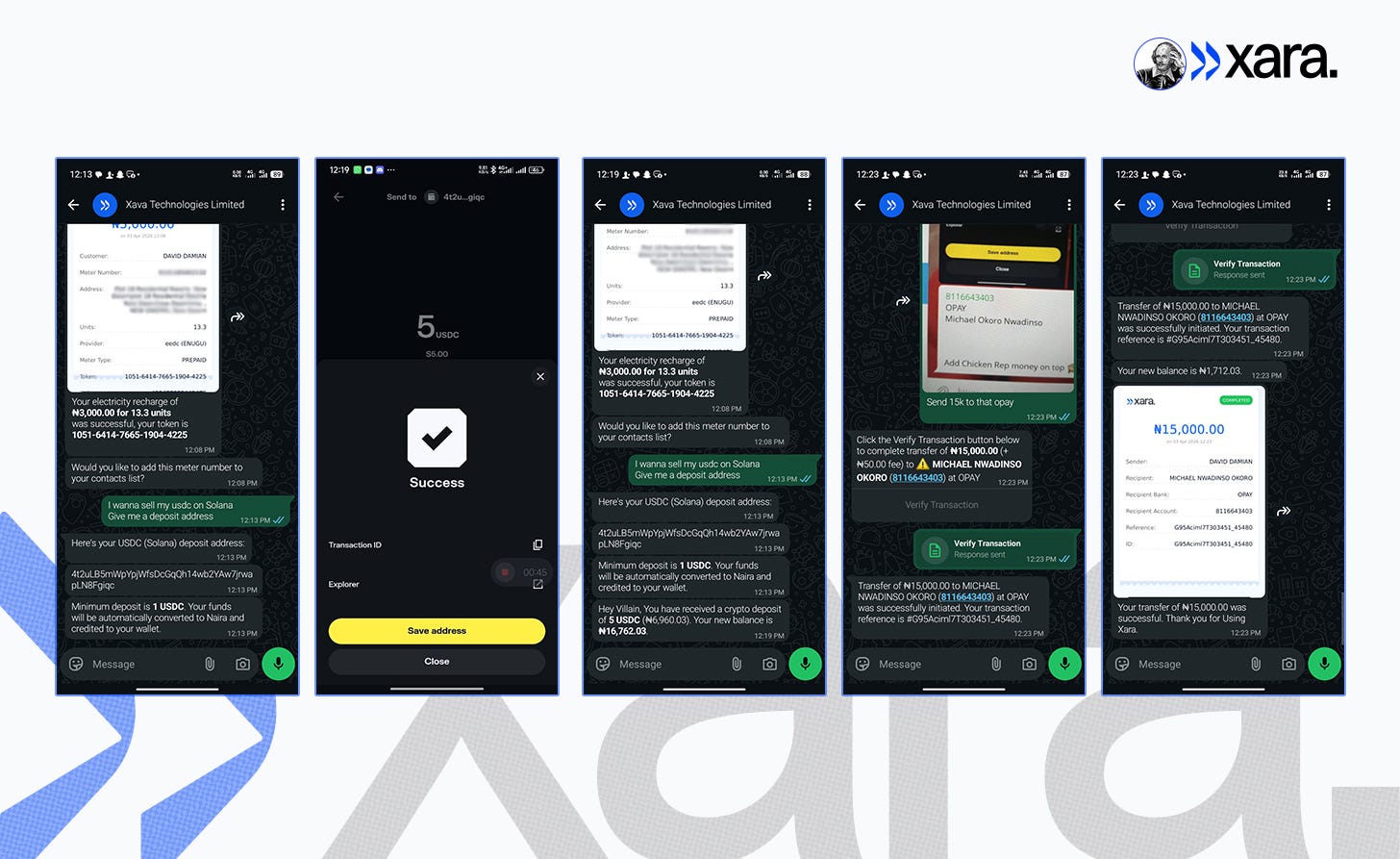

Test 5: Depositing and Off-ramping Solana Stablecoins (USDC & USDT)

No guide to Xara would be complete without testing its DeFi capabilities. For my final challenge, I decided to deposit and off-ramp stablecoins on the Solana network.

I began by telling Xara I wanted to sell my USDC and requested a deposit address. It provided one instantly.

Note: The minimum stablecoin deposit on Xara is currently $1.

I switched over to my Solflare wallet and transferred 5 USDC to the provided address. Xara confirmed the deposit almost immediately, automatically swapped it to Naira at the best available rate, and updated my balance within the same minute.

To wrap up the test, I took a photo of account details displayed on a nearby screen and instructed Xara to transfer ₦15,000 there. After a quick verification, the transaction was executed perfectly.

Verdict: By leveraging its Solana integration, Xara effectively transforms WhatsApp into a high-speed, seamless crypto-to-fiat gateway.

Bonus Test: Newly Released Feature

While finalizing this article, Xara launched a new feature that allows users to send money to another Xara user using only a phone number.47

Although my main tests had already been completed, I included this as a bonus test to reflect the latest product update.

Feel free to test it out on your Xara app by sending money to this number: 07044085646.

I’ll be waiting for your verdict. ;-)

5.0 FEEDBACK & INSIGHTS FROM FIRST-HAND USER EXPERIENCE

During the testing of Xara, four notable quirks were observed. Two of these were minor inefficiencies, while the remaining two created a degree of user discomfort. Let’s start with one of the minor inefficiencies which was a particular request that took Xara a full two minutes to complete, and might have taken even longer if I hadn’t stepped in.

After I bought airtime with Xara using the voice feature, it asked what name I would like to save the contact under. I used the voice note feature to record that I wanted it saved as Damian David Chidera, but I immediately changed my mind, retracted the statement, and said I would prefer it saved as Chainstellar instead. The voice recording can be heard below.

For a full two minutes, it seemed as though it was processing my request, as the three dots that appear when someone is typing on WhatsApp kept continuously showing. This continued until I sent a follow-up text message reiterating that I was still waiting for it to save the contact as Chainstellar. That was when it finally completed the request successfully.

You can confirm the timestamp in the first screenshot below, noting the gap between when I sent the recording and when it finally replied following my subsequent text. I later deleted the text to ensure the screenshot for an earlier section of this article looked clean, not realizing at the time I would need them for this feedback.

Now, this could be a one-time occurrence, but it highlights a potential limitation in the system’s ability to process revised instructions via voice input in real time. And it is possible that my initial recording lacked sufficient clarity, or that the system was unable to effectively reconcile the rapid change in user preference. Regardless of the underlying cause, the delay was still a letdown.

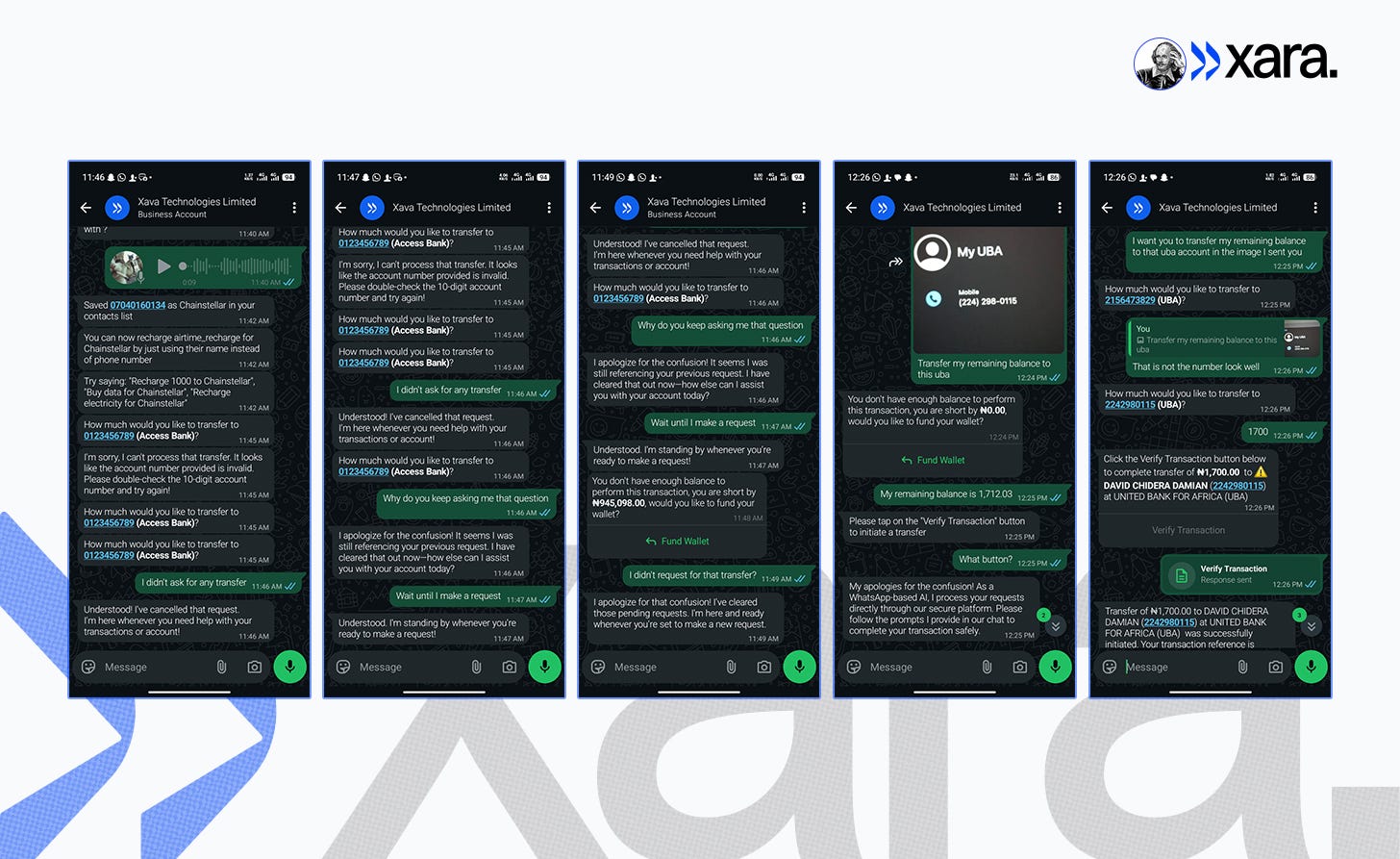

One of the critical issues occurred immediately after the airtime transaction. Xara began asking how much I wanted to transfer to a specific Access Bank account—a request I never made (see the first, second and third screenshots above). Despite repeatedly clarifying that I did not initiate any transfer, the prompts continued. At one point, it even asked me to fund my wallet, claiming I was short of ₦945,098.00 to complete a transaction I never requested.

Frustrated, I instructed it to transfer my remaining balance of ₦1,712.03 to an account number I had photographed on my laptop screen. It responded that I had insufficient funds and was short by ₦0.00. After I pointed out that I still had ₦1,712.03, it asked me to tap a “Verify Transaction” button that did not exist—marking the second minor inefficiency (see the fourth screenshot above).

Restarting the process, I again requested a transfer to the UBA account in the image I provided. However, it returned a different UBA account number, which was incorrect. This became my second critical issue. After prompting it to recheck, it finally displayed the correct account details. I then specified the amount again, verified the transaction, and the transfer was finally successfully completed (see the last screenshot above).

Notwithstanding the system’s early-stage irregularities, Xara demonstrates strong potential, with the ability to execute a wide range of complex and high-impact tasks accurately and reliably. Importantly, it does not autonomously initiate transactions that could directly compromise user funds, despite generating misleading prompts.

Nonetheless, the observed inconsistencies highlight the need for mandatory user verification and improved system reliability prior to broader deployment. Users should therefore carefully verify all transaction details before proceeding.

6.0 CONCLUSION

We have all heard the phrase “money talks,” but the problem is that only the rich could hear its voice.

In a way, Xara is not only making your financial lifestyle as seamless as having a conversation, but it is also giving the average person the opportunity to hear their money talk—for real. XARA IS WHAT HAPPENS WHEN MONEY TALKS FOR EVERYONE. Talk about true financial inclusion.

Xara provides a conversational layer to today’s financial infrastructure, integrating DeFi access powered by Solana. And it is on a path to becoming a WeChat-style super app, one place where users bank and interact with digital services, all through conversation.48

From cash to mobile money—every step improved access. Now comes the next shift: conversational finance. Be part of the evolution. Start using Xara today.