1.0 Background

Credit is the engine of wealth. Behind many giants of industry, there is usually a massive line of credit.

In his book Making It Big, billionaire Femi Otedola revealed that at the height of his financial crisis, he owed eight Nigerian banks a combined ₦222 billion: Access ₦25bn, Zenith ₦75bn, GTB ₦38bn, UBA ₦33bn, FCMB ₦26bn, Intercontinental ₦14bn, Union Bank ₦5bn, and Bank PHB ₦6bn.1

However, people often view borrowing as a sign of financial indiscipline. Many still assume debt is a trap. In reality, almost every worthwhile venture, from massive corporate empires to everyday infrastructure, is built on leverage. The wealthy rarely sell their assets to get cash; they borrow against them.

In Nigeria, credit flows almost exclusively through traditional banks. This model heavily favors large corporations, leaving millions of individuals and Micro, Small, and Medium Enterprises (MSMEs) stranded in a credit desert.

The Central Bank of Nigeria reported that private sector credit reached ₦75.8 trillion by late 2025. Yet, distribution remains deeply unequal. Nigeria’s credit-to-GDP ratio hovers around 12.9%, well below the Sub-Saharan African average of 20%.2

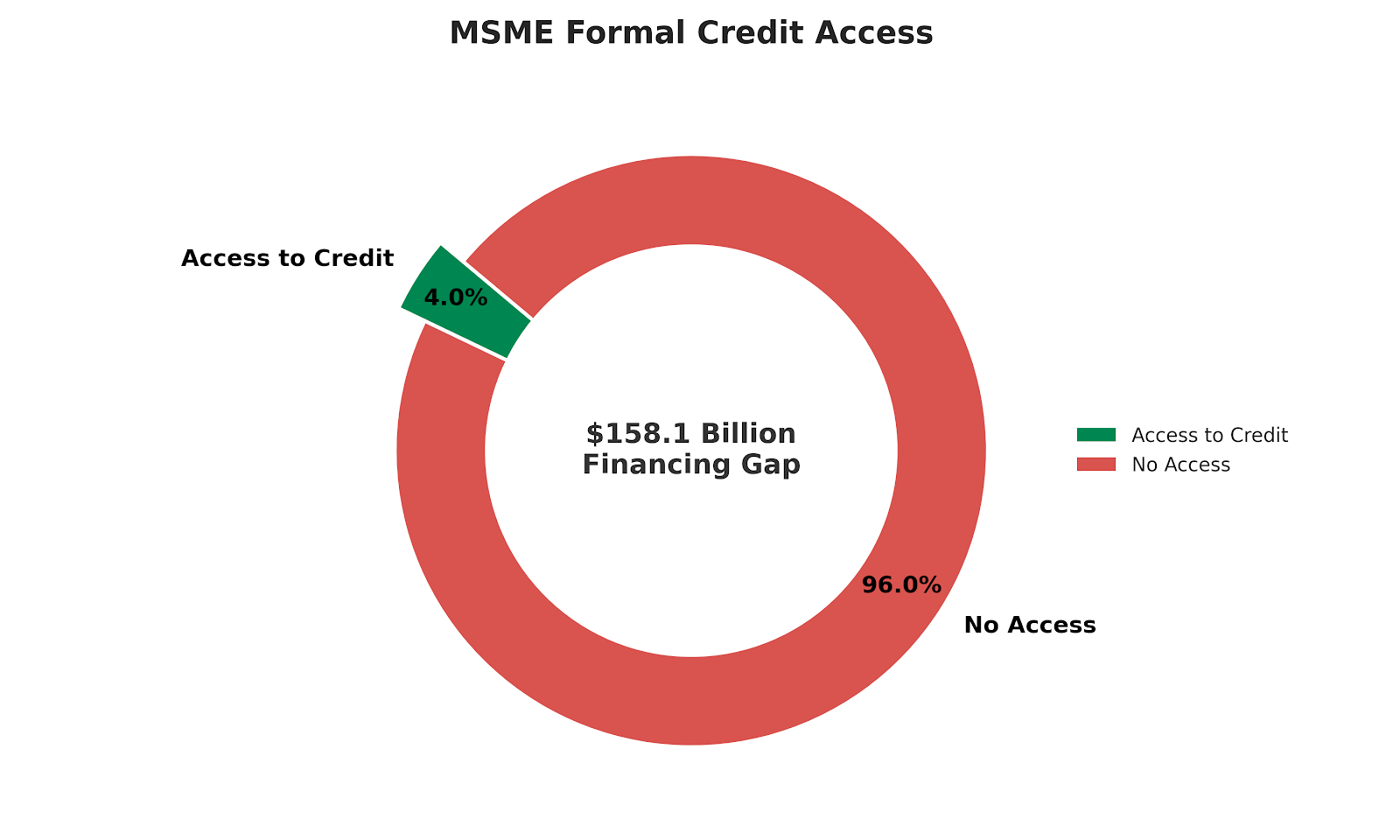

For the roughly 40 million MSMEs powering the nation, the situation is grim. According to The Guardian Nigeria, these businesses face a $158.1 billion financing gap, with less than 4% successfully accessing formal bank credit.3

The barriers are systemic. Banks demand physical assets like land for collateral, and the benchmark Monetary Policy Rate (MPR) recently hit 27.5%.4 At those rates, traditional borrowing becomes a growth killer for small businesses.

A figure like Femi Otedola can navigate these institutional hurdles using immense social leverage. But the average Nigerian is completely locked out of this ₦75 trillion credit pool. Solving this requires using decentralized assets to bypass centralized roadblocks and unlock immediate liquidity.

2.0 Instant Payment Growth: The Digital Proof Of Concept

Nigeria’s inaugural CBN Fintech Report (2026)5 documents an extraordinary expansion of real-time payments. It notes that “nearly 11 billion transactions were processed through the NIBSS Instant Payments (NIP) platform in 2024, up from five billion in 2022.” This 120% rise in just two years places Nigeria among the world’s fastest-growing adopters of instant payments.

More than 25% of all Nigerian electronic transactions now run on real-time rails,6 and the country leads Africa in total NIP volume. These trends reflect a sustained growth of digital finance: industry sources project Nigeria’s domestic payments revenue to rise ~34% annually through 2026, driven largely by online and card-based transactions.7

2.1 2023 Cash Redesign as a Tipping Point

Data and analysis indicate that the Central Bank’s October 2022 decision to redesign major naira notes was the precipitating “tipping point” for digital uptake. When old notes were invalidated in early 2023, Nigeria faced a severe cash crunch. Consumers and small businesses, especially the largely informal 90%-of-economy segment, responded by adopting digital payments en masse.

After the 2023 naira redesign, POS deployments jumped dramatically, 2024 saw 116.8% growth, adding 3 million terminals.8 This expansion to 5.5 million devices in 2024 shows how businesses raced to enable card/mobile payments amid the cash shortage.

Fitch and NIBSS report that the scarcity of physical naira became a “significant catalyst to the adoption of digital financial services.” 9 Indeed, CBN statistics show NIP volume soared:

5.626B instant transfers were recorded in H1 2024 (16% higher than H2 2023).10

POS usage spiked: Deployed terminals rose 20% in early 2024, and transaction counts jumped 29% in volume.10

This shift was powered by the infrastructure of Mobile Money Operators (MMOs), companies like OPay, PalmPay, and Moniepoint. By deploying millions of POS terminals and mobile agent networks, these providers bridged the gap where traditional banks failed. By late 2025, Moniepoint reported handling a staggering 80% of Nigeria’s in-person payments,11 processing ₦412 trillion in transaction value, while PalmPay recorded 15 million daily transactions.12

EFInA’s Access to Finance survey shows that formal inclusion rose to 64% in 2023, driven heavily by this fintech adoption.13 Nigerians have already proven they will abandon legacy banking for pure efficiency. When a system is fast, transparent, and works on a smartphone, the average person gains the agility to move capital like the financial elite.

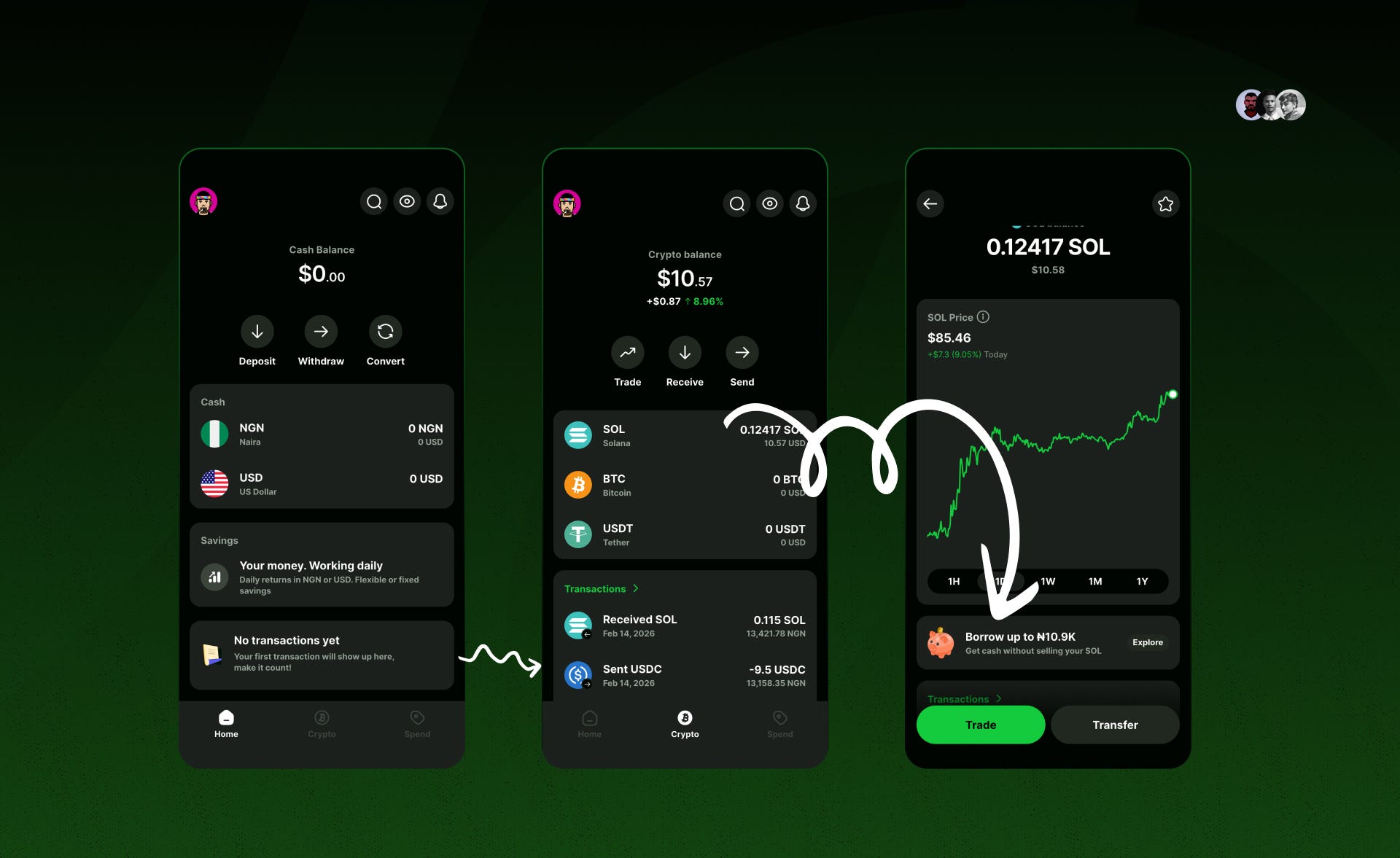

3.0 Enter Busha

Launched in 2019, Busha focuses on the Nigerian and Kenyan markets. It has evolved from a basic cryptocurrency exchange into a comprehensive financial platform that bridges the gap between traditional fiat and digital assets.

In January 2026, the platform launched Busha 3.0, expanding its services to include tokenized real-world assets, advanced business tools, and Asset-Backed Loans.

Specifically, it introduced Solana (SOL) backed loans, allowing users to tap into fiat liquidity without selling their crypto.

The real innovation that sets it aside is accessibility. On-chain borrowing is not new. Solana DeFi protocols like Kamino and MarginFi have offered it for years, but the barrier to entry is high friction. Getting a loan directly on-chain requires connecting a wallet, approving token spending caps, depositing collateral, paying gas fees, executing the borrow, paying more gas fees, and bridging the funds to an off-ramp for Naira. That creates a heavy cognitive load.

Busha acts as an abstraction layer, bundling those complex interactions into two clicks. It leverages the speed and liquidity of the Solana blockchain and wraps it in an interface that completely removes the headache of self-custody management. You get DeFi execution speeds alongside neobank usability.

MMOs proved Nigerians are ready for digital-first payments, and Busha is testing if the market is ready for asset-first credit. Just as mobile money bypasses the physical queues of traditional banking halls, Busha 3.0 bypasses the collateral trap of legacy loans.

If you trust your phone to pay for lunch, you can trust your Solana to fund your business.

3.1 Why Do Busha Solana-Backed Loans Matter?

I recently discussed Busha's SOL-backed loans with a friend outside the crypto space. He replied with four core questions:

a. Why borrow money if you already have SOL?

Let’s indulge in a thought experiment and picture yourself as Otedola. If you needed 800 million Naira urgently but didn’t have that amount in liquid cash, you would likely have that value in assets. Would you rather sell those assets or borrow against them? The answer is mathematically obvious.

The same logic applies to digital assets. Think of your Solana like land in a rapidly developing neighborhood. Selling it to fund a short-term need means you lose out completely when the area’s value goes up. Borrowing gives you cash now while keeping your stake in the asset.

Upside Exposure: If you borrow against your SOL and the price jumps from $100 to $200, you still own the asset. You get the cash you need today and capture the profit tomorrow. That profit can potentially pay off the loan entirely (Not Financial Advice).

Tax Efficiency: Selling crypto for profit triggers a 10% Capital Gains Tax under Nigeria’s 2026 regulations.14 Taking a loan is not a sale and avoids this taxable event.

Speed: Securing a local bank loan involves endless paperwork and weeks of waiting. A Busha loan is instant.

The “Naira Short” (Inflation Arbitrage): In an economy dealing with 30% inflation, holding cash guarantees a loss of purchasing power. Borrowing against your SOL effectively shorts the Naira. You spend fiat today at its current value and pay the loan back later with fiat that is statistically worth less. The 2% monthly interest is often absorbed by the currency’s devaluation.

The P2P Sniper: Markets operate 24/7, but P2P liquidity fluctuates. During weekend panic dips, P2P spreads widen. You might find yourself selling at ₦1,400/$ when the global market sits at ₦1,450/$. Instead of selling your SOL at a desperation rate for urgent cash, you can take a Busha loan instantly to pay your bill. You wait for P2P rates to normalize on Monday, then sell a much smaller fraction of SOL to clear the debt.

b. What If Solana Drops?

Borrowing against volatile assets carries downside exposure as well. Platforms manage this risk using a Loan-to-Value (LTV) ratio.

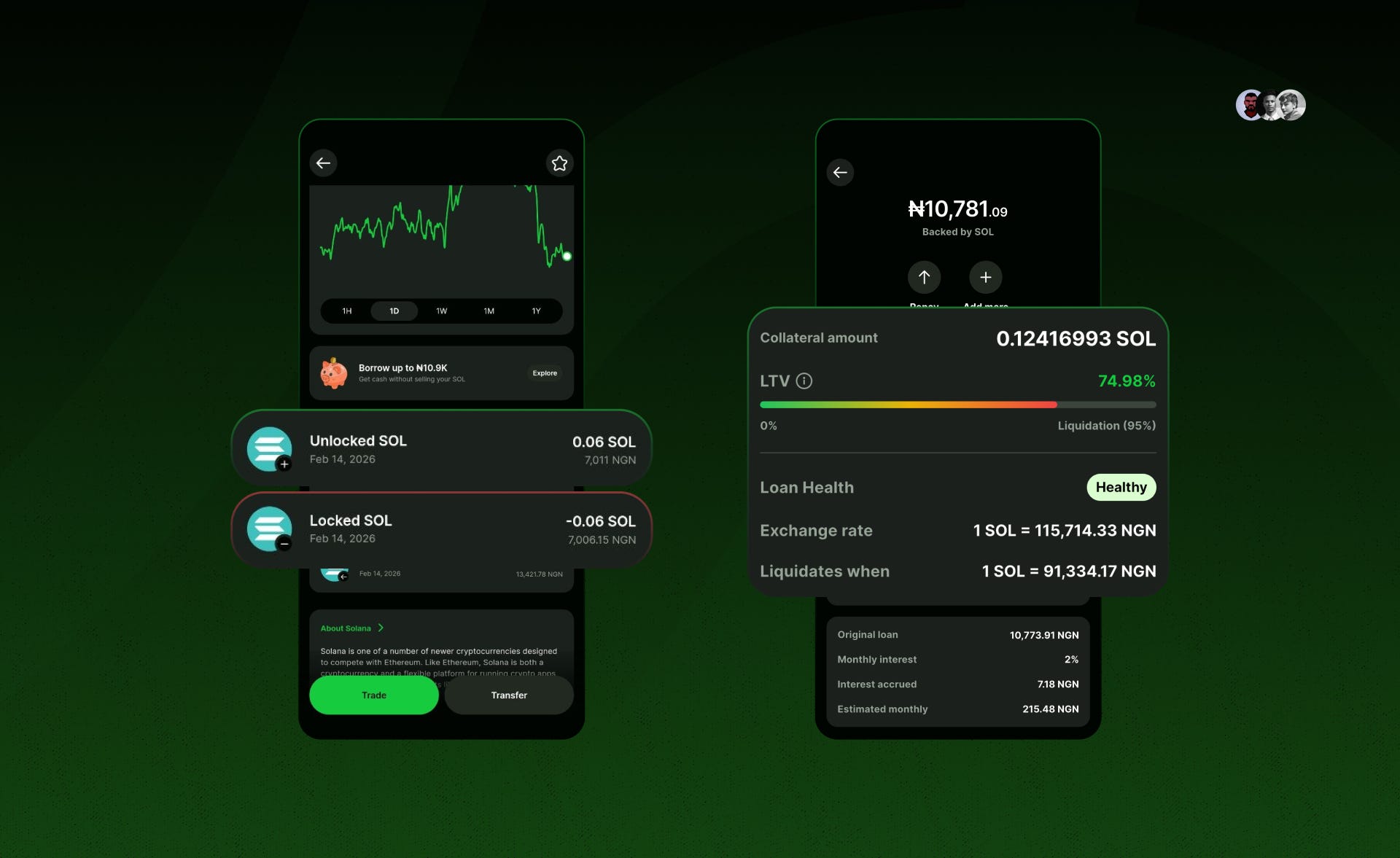

Think of LTV as the health meter for your loan. It tracks the balance between the cash you borrowed and the current market value of your locked Solana. You calculate it by dividing your borrowed amount by the current value of your collateral. If you borrow ₦750,000 against ₦1,000,000 worth of Solana, your starting LTV is 75%. Liquidation threshold is at 95%, so you have a 20% buffer which acts as a safety cushion.

If Solana’s price falls, your collateral loses value, automatically pushing your LTV percentage higher. When it climbs into the warning zone of 80% to 90%, Busha triggers a Margin Call via email and push notification. You can fix your health meter by depositing more Solana to boost your collateral value, or by paying back a portion of the loan to reduce your debt.

If the market crashes sharply and your LTV hits the 95% liquidation threshold, the platform automatically sells enough of your Solana to settle the outstanding debt. You keep the cash you originally borrowed, but you lose that specific portion of your digital assets.

c. Why is the borrowing limit capped at 75%?

This cap is a built-in protection mechanism. If the platform allowed a 95% borrow limit right away, a minor market dip would liquidate your position instantly.

Limiting your maximum borrowing power to 75% guarantees a solid 20% LTV gap before you hit the 95% liquidation threshold. You have plenty of time to react to market swings before forced selling occurs.

d. What is the interest like on Busha?

Busha 3.0 charges a 2% monthly interest rate on the borrowed amount. Unpaid interest is added to your total debt.

For an appreciating asset like Solana, whe the price takes off, your Loan-to-Value (LTV) ratio improves because you now have more collateral value backing your debt. In a scenario like this, you actually have the flexibility to borrow more against your existing loan.

Interest will continue to accrue at that same 2% monthly rate, but you’re always in control. You can repay your loan, in part or in full, whenever you like, provided your collateral remains comfortably above the LTV requirements.

When you’re ready to close things out, you’ll simply pay back the outstanding loan balance plus any accumulated interest. Just keep in mind that if the market dips or interest builds up, you’ll have slightly less Solana backing the same loan, causing your LTV percentage to creep up over time.

4.0 Visual Walkthrough On How To Obtain A Loan On Busha Using Solana

Before making this in-app walkthrough, I audited the loan engine with real funds to verify the settlement speed and risk logic. I deposited 0.12 SOL and requested a loan of ₦5000, which is the minimum amount you can borrow. Here is how the engine performed behind the scenes:

Isolated Margin Safety: Many crypto lenders aggressively lock your entire wallet balance as collateral. Busha’s engine calculated the exact collateral needed to secure my specific loan (0.06 SOL) and partitioned it. My remaining 0.06 SOL remained unlocked and liquid. This isolated margin approach ensures a single active loan will not freeze your entire portfolio.

The 75% Efficiency Standard: The app defaults to a starting Loan-to-Value (LTV) of exactly 75%. This reveals the engine’s philosophy of capital efficiency. Rather than over-collateralizing and locking up too much of your SOL, the algorithm isolates the exact minimum required to dispense your cash.

The 95% Safety Net: Starting an isolated chunk at 75% LTV leaves a solid 20% gap before hitting the 95% liquidation threshold. Most DeFi protocols liquidate at 85%. Pushing this threshold to 95% provides a generous buffer before forced selling occurs.

The Latency Result: I clicked borrow at 5:11 PM. The Naira was spendable in my wallet at exactly 5:11 PM. Zero lag. This is programmatic settlement.

4.1 How to Execute

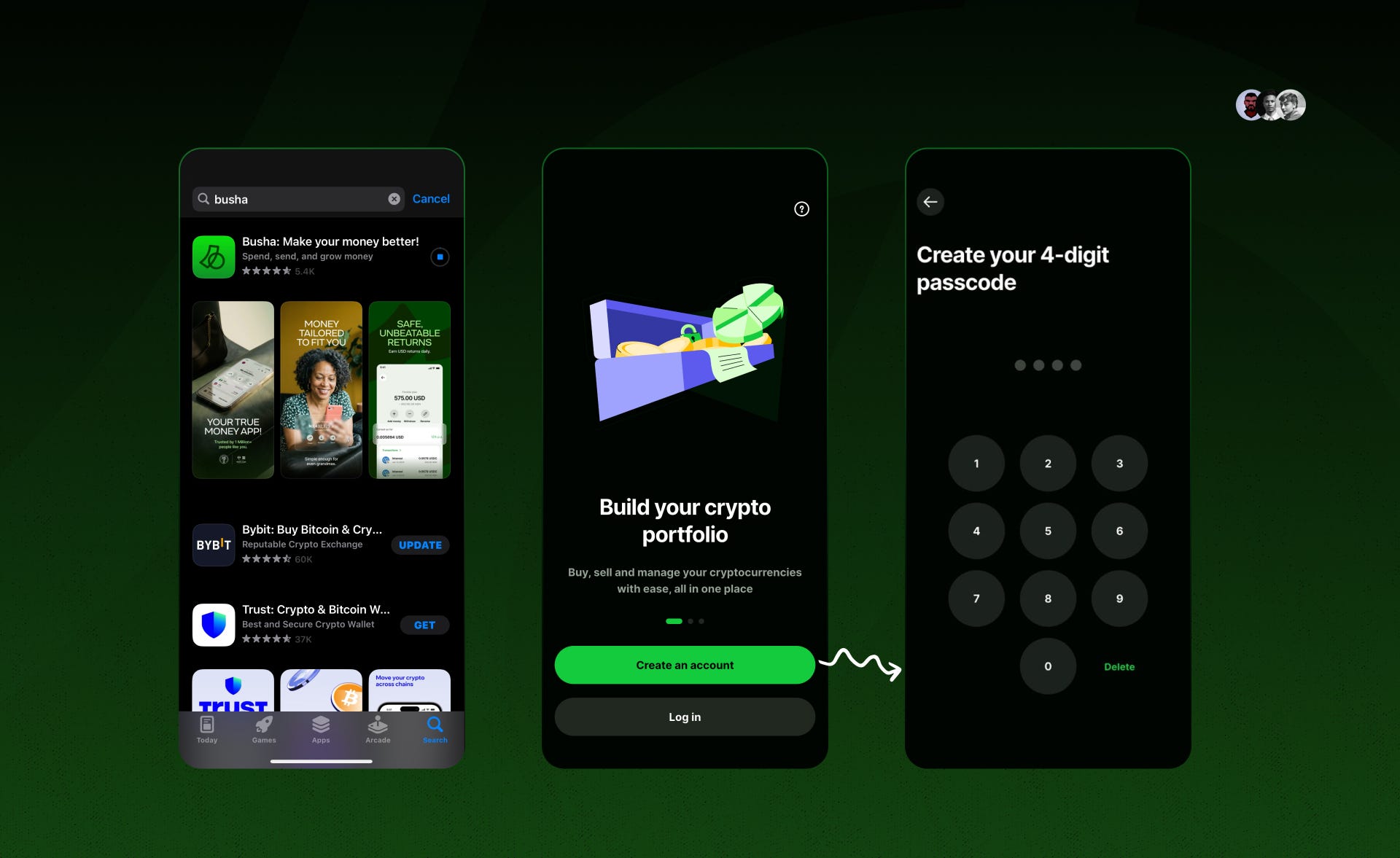

Step 1: Download the App

Search for Busha on the Google Play Store or Apple App Store and install it.

For iOS: Busha on the App Store

For Android: Busha on Google Play

Step 2: Sign Up or Log In

Launch the app. Select Create an Account if you are a new user, or Log In if returning.

Step 3: Secure Your Account

Complete your identity verification (KYC). This involves linking your phone number and email, providing a government-issued ID or BVN, and enabling Two-Factor Authentication (2FA).

Step 4: Navigating the Interface

The Busha 3.0 update organizes the app into three primary navigation tabs:

Home: A unified view of your local fiat currency and stablecoins.

Crypto: Where you manage and trade digital assets like Bitcoin and Solana.

Spend: For daily utility, allowing you to pay for essentials like airtime and data.

To start your loan, navigate to the Crypto tab. Select Buy SOL, or hit Deposit to move assets from another wallet. Make sure it’s at least $10 worth of SOL, as this is the minimum amount you can borrow against. Tap the Solana asset icon, scroll to the bottom of the page, and click the Borrow feature.

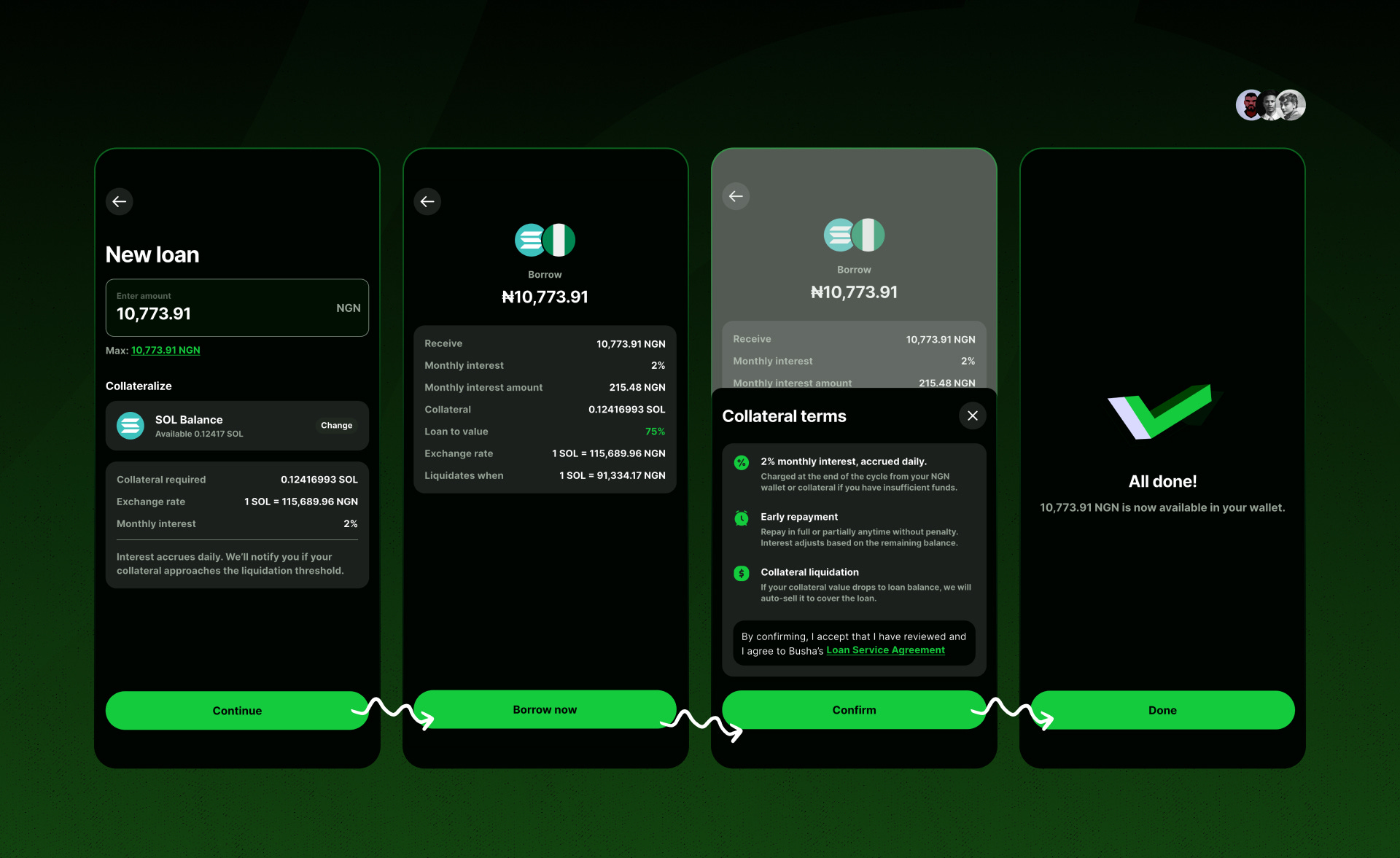

Step 5: Finalize and Confirm

Enter the amount of Naira you wish to borrow. The app calculates the maximum available amount based on your collateral, allowing you to borrow up to 75% of the current value of your deposited Solana.

Review the loan details, noting the 2% monthly interest rate, liquidation price, and your starting LTV. Click Confirm. The funds will appear in your Naira wallet instantly.

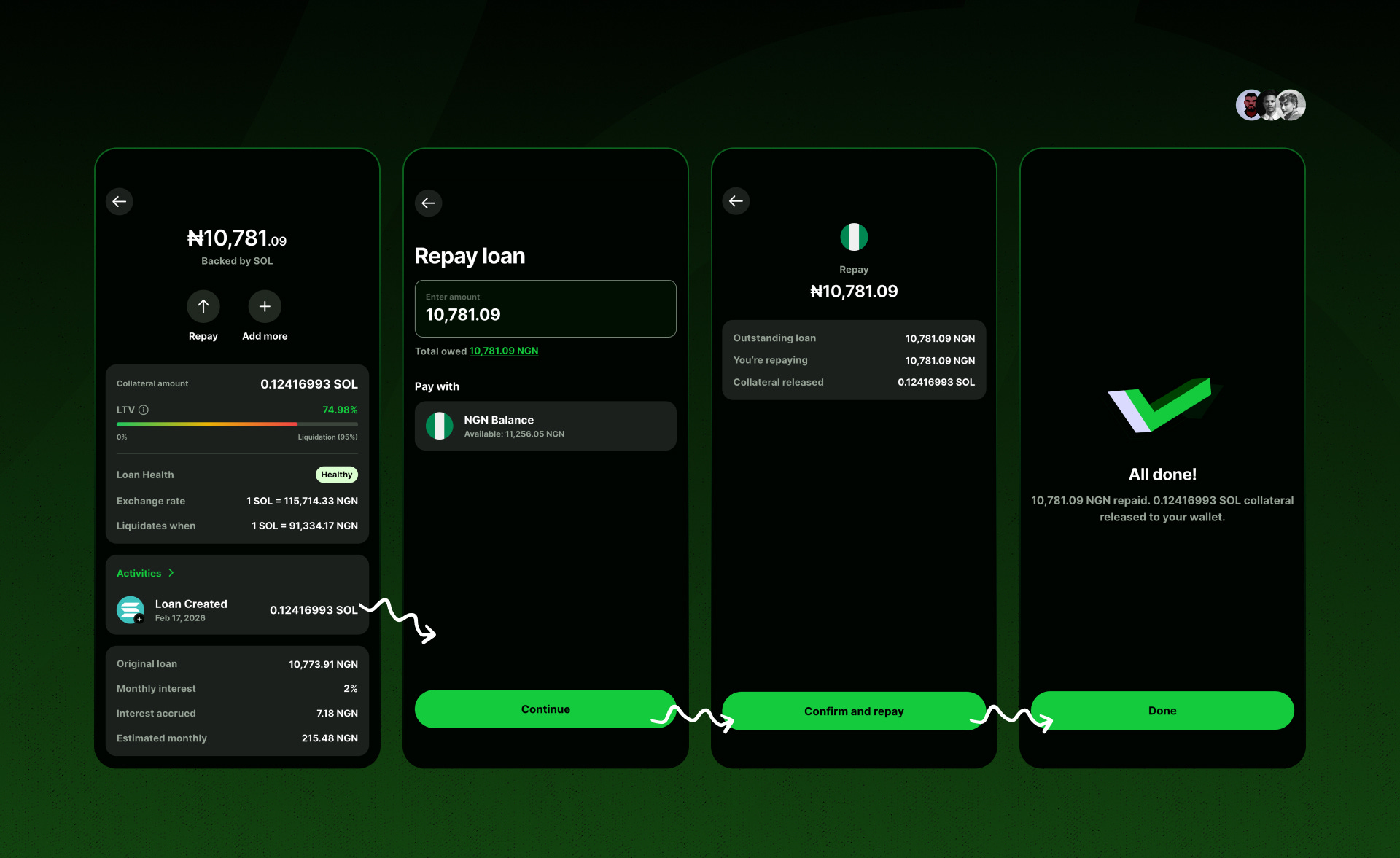

Step 6: Repaying Your Loan and Reclaiming Your Collateral

Go to your Naira wallet on the Home tab to locate your outstanding loan. Tap the balance and click Repay.

You can make a partial payment or settle the full debt at once. Once confirmed, your Solana collateral is immediately unlocked and returned to your main Crypto wallet.

While Busha’s interest rate is quoted as 2% per month, it accrues on a daily basis. You only pay for the exact time you hold the loan.

For instance, I borrowed ₦10,773.91 for the walkthrough and repaid it within minutes, I paid ₦10,781.09. A 2% monthly interest rate on ₦10,773.91 is ₦215.48 and divided by 30 days, that is exactly ₦7.18 per day.

5.0 Feedback & Insight From First-Hand User Experience

While the Busha 3.0 experience is largely seamless, I noticed a few platform quirks during my run.

The instant Convert feature on the crypto tab currently only supports three main assets: BTC, cNGN (Compliant Naira), and USDT.

I deposited USDC intending to swap it directly for Solana, but SOL was missing from the direct convert menu. You’ll have to stick with depositing and buying SOL directly for now.

However, on the Home tab, you can still deposit Naira and convert it to Solana directly.

Additionally, the Borrow feature is a mobile-only tool. The web version of Busha is robust for trading and tracking your portfolio, but you will need your phone to access credit.

5.1 The 60-Second Loop: A Note on Cost vs. Value

To test the platform’s real-world cost, I executed a “60-second loop.” I borrowed ₦10,918, held it for exactly one minute, and then repaid it. The interest charged was ₦7.28, bringing the total repayment to ₦10,925.

Because the system operates on a 2% monthly interest rate, the cost is broken down to roughly 0.06% per day, any transaction incurs a minimum charge of one day’s interest. While this is a technical “floor,” it reveals a massive strategic advantage for traders: the cost of instant capital is negligible.

Consider the utility for a business owner:

The Scenario: A vendor offers a ₦5,000 “flash discount” for an immediate cash payment.

The Cost: If you don’t have the cash on hand, you can borrow it instantly. Even if you hold that debt for three days, the interest might only cost you ₦200.

The Result: By spending ₦200 in interest, you secure ₦5,000 in savings.

In this context, debt isn’t a burden, it’s a profit-generating tool. For the price of a single stick of gum, you can unlock ₦10,000 worth of instant liquidity to capture opportunities that would otherwise be missed.

6.0 Conclusion

The modern financial engine is highly efficient at catering to the needs of billionaires like Femi Otedola. This exposes a massive gap in how capital is distributed. The vast majority of MSMEs and everyday Nigerians are left stranded in a credit desert, forced to liquidate their hard-earned assets just to cover immediate expenses.

The phrase ‘it is more expensive to be poor’ is factual, as the true power the elite hold over the average person lies in leverage and accessibility, two structural benefits that even liquid assets or money alone cannot always guarantee.

I personally deposited ~$20 worth of Solana and accessed instant liquidity. This would be impossible in the traditional banking sector. When we cut down the blockages between capital and the average user, we don’t just “bank the unbanked”, we empower them. Busha is bridging the gap between the privileged and the underprivileged by using decentralized finance to fix the inefficiencies of the current structure.

Do not sell your future to pay for today’s liquidity needs. Use Busha 3.0 to borrow against your Solana, maintain your market upside, and keep your capital working for you.

7.0 References

CBN to Convene 304th MPC Meeting on February 24 to Review Interest Rates

Nigeria saw an increase of 2.9 million deployed POS in 2024, following the naira redesign in 2023

Nigeria’s cash crisis provides boon for fintech and mobile money operators, Fitch reports

Report: Moniepoint says it handled 80% of Nigeria’s in-person payments in 2025

EFinA Report: Nigeria’s Formal Financial Inclusion Grows to 64% in 2023

Nigeria set to tax individual crypto transactions and exchanges in 2026