1.0 Background

On January 21, 2026, popular streamer IShowSpeed arrived in Nigeria as part of his Africa tour. Amid massive fan crowds in Lagos, he celebrated his 21st birthday and visited a local jewelry store to purchase 18-karat diamond earrings.

When traditional payment methods like Apple Pay, Zelle, CashApp and Venmo proved unavailable,1 he completed the transaction using USDC & USDT. While this perfectly demonstrates real-world stablecoin utility, especially in a country where global payment rails are often inaccessible, it remains a highly uncommon occurrence.

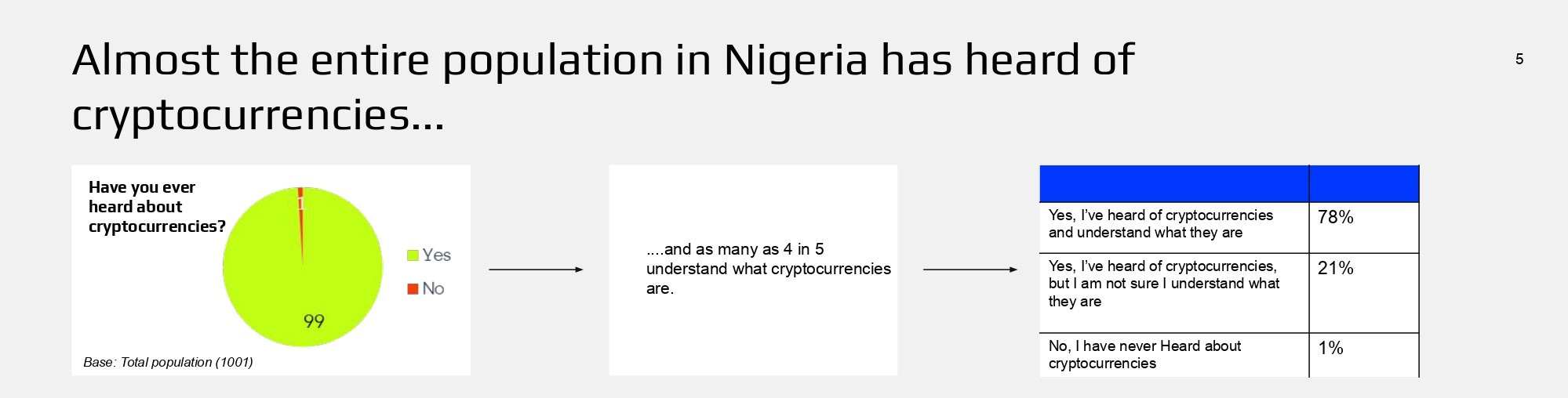

Nigerians are deeply familiar with crypto. A 2023 Consensys/YouGov global survey shows that 99% of Nigerians are aware of cryptocurrency,2 and 78% claim to understand it.3 However, adoption data reveals that this conceptual awareness rarely translates into functional utility. Only about a quarter (25.1%) of Nigerian crypto users employ digital assets for routine transactions,4 with the majority citing a lack of practical understanding as the primary barrier.5

By 2025, an estimated 22 million Nigerians, representing roughly 10.3% of the population, owned or used cryptocurrencies.6 Yet, on the retail level, adoption is heavily investment-led. Digital assets remain locked away as instruments for speculation or long-term storage instead of operating as spendable currency. In many cases, they are still treated as a high-risk sandbox for everyday finance.

Our findings reveal that Nigerian crypto adoption on the retail level is fundamentally investment-led. While international observers often focus on crypto’s role in cross-border payments and remittances, the local reality is far more sophisticated.7

Stablecoins have evolved far beyond a niche “Nigerian hack” for a failing Naira. The global financial system is rapidly shifting toward an always-on internet economy where digital dollars are the preferred medium of exchange. According to the 2026 Circle Strategic Report, on-chain USDC transaction volume grew by a staggering 680% in 2025, hitting nearly $10 trillion in a single quarter.8 Nigeria currently leads Sub-Saharan Africa in raw volume,9 but other regions are already providing the roadmap for how stablecoins function as everyday infrastructure.

Take Brazil, which has emerged as a gold standard for adoption. Over 90% of the country’s crypto activity is now stablecoin-related. Neobanking giants like Nubank10 and Mercado Pago have integrated USDC directly, allowing over 100 million users to save and spend as easily as they would with local currency.11 Similarly, in Argentina, fintechs are issuing Visa-branded crypto debit cards that automatically convert stablecoins to pesos at checkout,12 driving massive consumer uptake.

Collectively, these regions demonstrate a clear reality. When stablecoins are treated as cash, they unlock a level of financial inclusion that Nigeria is only just beginning to tap into.

2.0 Why Are Nigerians Underusing Stablecoins Despite Their Situational Fit?

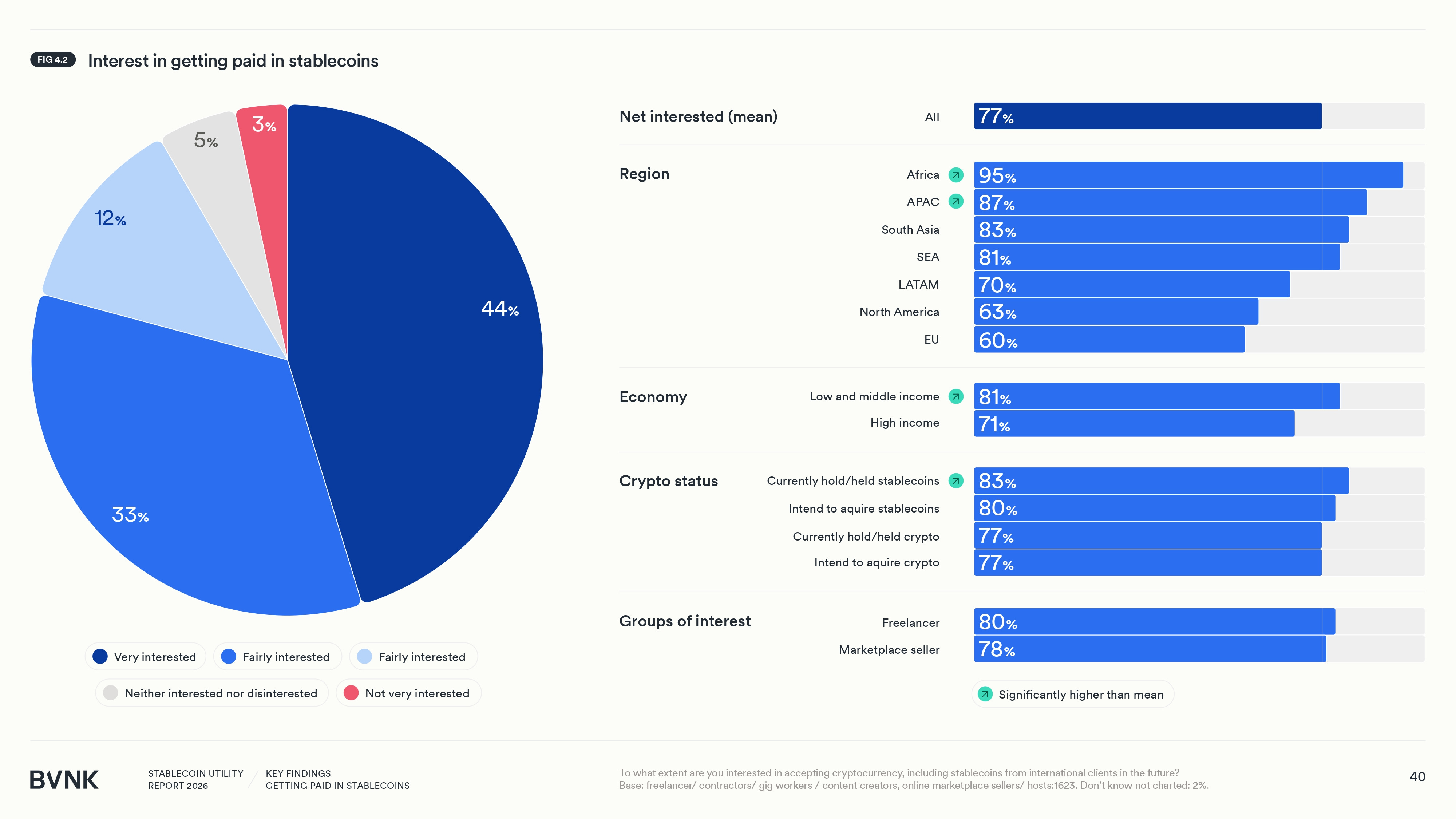

Nigeria’s economic reality—a volatile Naira, high inflation, costly remittances, and uneven banking access—creates the perfect environment for digital dollars. Yet, everyday stablecoin use remains remarkably low. A BVNK Stablecoin Utility Report 2026, in partnership with YouGov, Coinbase and Artemis, revealed that 95% of African respondents actually want to be paid in stablecoins instead of their local currency.13 However, consulting firm BCG estimates that only about 6% of stablecoin transactions in Africa are for goods or services,14 while roughly 90% are purely for crypto trading.15

This disconnect is reflected across multiple studies. According to an Intelpoint report based on Quidax’s State of Crypto Adoption in Nigeria 2025, 67.2% of Nigerian crypto holders use their assets primarily for investment. Only 18.4% use them for everyday needs like payments or remittances.16 The latent demand for dollar stability is massive, but transforming that demand into routine transactions is blocked by four core barriers:

Regulatory and policy barriers:

The 2021 circular issued by the Central Bank of Nigeria (CBN) severed crypto from the formal banking system, leaving many Nigerians with frozen accounts.17 Although the ban was formally lifted in December 2023,18 the reputational damage and legal ambiguity linger. In late 2025, the CBN formed a “task force” to study stablecoins19 – a clear sign the government still views them as exotic instruments. Simultaneously, new frameworks taking effect in 2026 will heavily tax crypto profits, with gains on digital asset transactions facing up to a 25% levy.20 Exchanges are now mandated to report user trades to tax authorities. This ongoing policy uncertainty, coupled with retrospective taxes, naturally deters risk-averse Nigerians from treating crypto as spendable cash.

Knowledge, Trust, and Safety Issues:

Awareness does not equal comprehension. Adoption data from TGM StatBox shows that 65.64% of Nigerians cite a lack of understanding as a major barrier to using crypto daily.21 Scams and volatility remain global entry barriers,22 but the local psychology is highly specific. Academic research published by Cambridge Research and Publications, authored by Dr. Obiefule, Harrison Chinonso, found that perceived security and stability are by far the strongest drivers of Nigerian adoption. Everyday utility mattered much less in the data.23 The takeaway is clear. Nigerians will only spend stablecoins if they feel the underlying infrastructure is entirely safe and reliably stable.

Infrastructure and Acceptance Gaps:

Even willing users cannot spend what merchants refuse to accept. Most Nigerian shops, online services, and billers expect Naira through established digital payment channels; very few integrate crypto wallets. The BVNK Stablecoin Utility Report highlights limited merchant acceptance as a primary bottleneck for retail crypto use. Users want to hold and spend stablecoins, yet everyday merchant off-ramps are still missing.24 This directly correlates with the data showing only ~6% of African stablecoin transactions are for payments. When combined with developing-market hurdles like uneven smartphone penetration and spotty internet in rural areas,25 crypto activity is largely restricted to urban youths. Until local payment rails become crypto-native, stablecoins will remain a fringe spending tool.

Social and Cultural Factors:

Crypto in Nigeria has long suffered from a purely speculative image. Many still view assets like Bitcoin and Tether strictly as speculative vehicles to stash dollars or generate quick wealth. The 2021 regulatory crackdown reinforced a narrative equating crypto with illegality, heavily undermining its credibility for daily use. Dr. Obiefule, Harrison Chinonso study noted that social acceptability actually had a negative effect on adoption,26 suggesting Nigerians make stablecoin decisions based on personal risk-reward calculations rather than following the crowd. Consequently, routine transactions like school fees, groceries, and utilities are still routed through trusted cash, bank transfers, or familiar fintech apps.

Nigerians are underusing stablecoins despite an overwhelming need. We desperately want the stability of the dollar, but we are boxed in by a wall of friction. To transition crypto from a static investment into everyday spending, we need a fundamentally new financial playbook that strips away the complexity and treats stablecoins exactly like cash.

3.0 Enter Finna

Finna redefines what a crypto app should be. It operates as a utility bridge explicitly designed to bypass the layers of friction stifling Nigerian stablecoin adoption.

The existing utility gap proves that simply knowing USDC and USDT exist isn’t enough. The hurdle is infrastructure. You shouldn’t have to be a global superstar or shop at luxury stores to pay for everyday needs with digital dollars.

Finna brings that seamless experience to every Nigerian with a smartphone.

In January 2026 alone, Finna processed over $6 million in transaction volume, proving that Nigerians are actively adopting this new, Solana-powered playbook.27

Play 1: Solving the Infrastructure & Acceptance Gap

The primary bottleneck for the average user is straightforward. You cannot pay for groceries, a Bolt ride, or school fees directly from a Phantom wallet.

While direct merchant acceptance of crypto hovers around a dismal 6%, Finna users bypass this limitation entirely by treating the platform as a frictionless liquidity engine. For routine weekly expenses, users can instantly swap USDC to Naira and off-ramp to their local bank for a flat ₦100 fee, completely bypassing the steep spreads and delays of P2P markets. For larger liquidity needs, Finna solves this by allowing users to keep their wealth in USDC while instantly borrowing Naira against it, preserving their long-term hedge against Naira devaluation.

This effectively makes a stablecoin balance spendable anywhere Naira is accepted, completely eliminating the need to find a crypto-native merchant.

Play 2: Finna As a Regulated Ecosystem

The fallout from the 2021 CBN ban left millions of Nigerians reliant on opaque, high-risk P2P channels.

Finna addresses this foundational trust barrier by operating as a formal, secure fintech entity. By providing a licensed lending environment, Finna transforms stablecoins from exotic, speculative tokens into legitimate financial collateral.

This shift not only gives the user peace of mind but forces digital assets to speak a language that both local laws and traditional banks understand.

Play 3: Bridging the Knowledge & Social Gap

Although most Nigerians are aware of cryptocurrency, many lack the practical knowledge required to use DeFi tools confidently, resulting in a clear awareness and utility gap.

Finna’s strategy is simple as it strips away the jargon and complexities of DeFi. It markets familiar banking behavior like Lending, Deposits and Transfers.

Finna eliminates the copy-paste anxiety that comes with having a string of intimidating 44-character wallet addresses. Instead, you can get paid using your unique Finna Tag (username) and receiving and sending USDC/USDT becomes as intuitive as an OPay transfer.

With this innovation, Finna overcomes the cultural inertia that keeps people stuck in traditional, inflation-prone banking.

Play 4: Eliminating Cost And Friction via Solana

Legacy blockchains like Ethereum or Tron are structurally incapable of handling routine Nigerian micro-transactions due to high cost and congestion. While Finna supports stablecoin deposits across multiple networks to ensure widespread accessibility, it solves daily transaction friction by powering its core internal ecosystem on Solana. This integration provides three non-negotiable benefits:

Cost: Solana’s base fees are fractions of a cent. This means a user can move $5 or $5,000 without network “gas” cannibalizing their working capital.

Speed: Operating with block times of around 400 milliseconds, a cross-border Finna transfer settles with the exact same instantaneous feel as a domestic NIP bank transfer.

Reliability: Traditional financial systems frequently buckle under peak-hour congestion, resulting in hanging transactions. Solana is engineered for continuous uptime. With 2026 network upgrades like Firedancer28 delivering institutional-grade throughput, the infrastructure guarantees that whether you are the first user or the 100-millionth, the settlement remains instant, secure, and deterministic.

4.0 Visual Guide: Using Finna’s Products

I’m going to walk you through the three core Finna features you need to know: how to get a stablecoin-backed loan, how to set up and send money using just a Finna username, and finally, how to withdraw your Naira or stablecoins directly to your bank account. But first, we need to download and set up the app.

Step 1: Download the App

Head over to your Play Store or App Store and search for “Finna” to install it. Alternatively, you can use the web app if you prefer a desktop experience.

For iOS: Finna on the App Store

For Android: Finna on Google Play

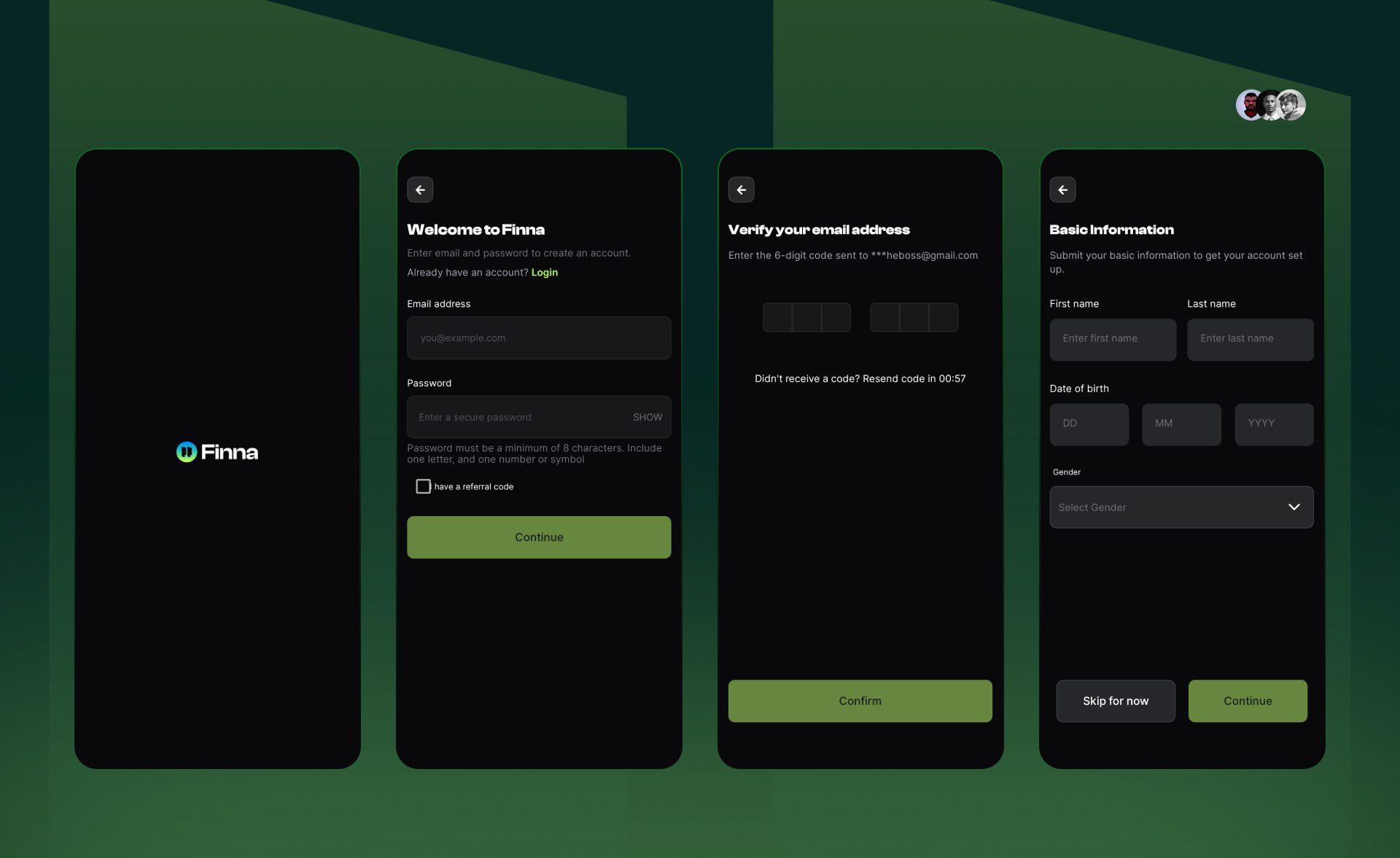

Step 2: Sign Up or Log In

Launch the app. Select Sign Up if you are a new user, or Log In if returning.

Step 3: Secure Your Account

Complete your identity verification (KYC). This involves inputting your email address and verifying it, providing basic information like name, date of birth and gender.

Step 4: Complete Your Identity Verification

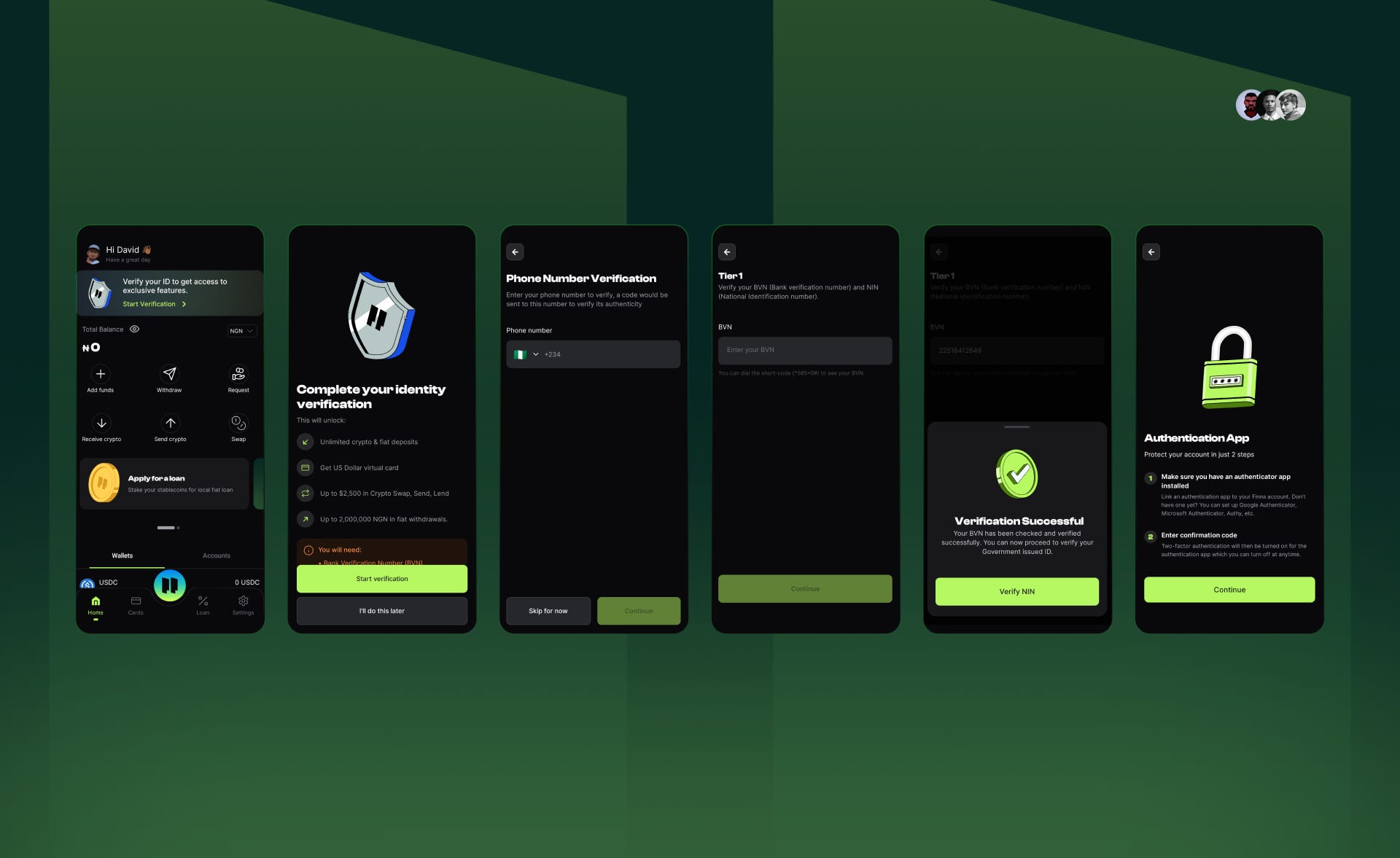

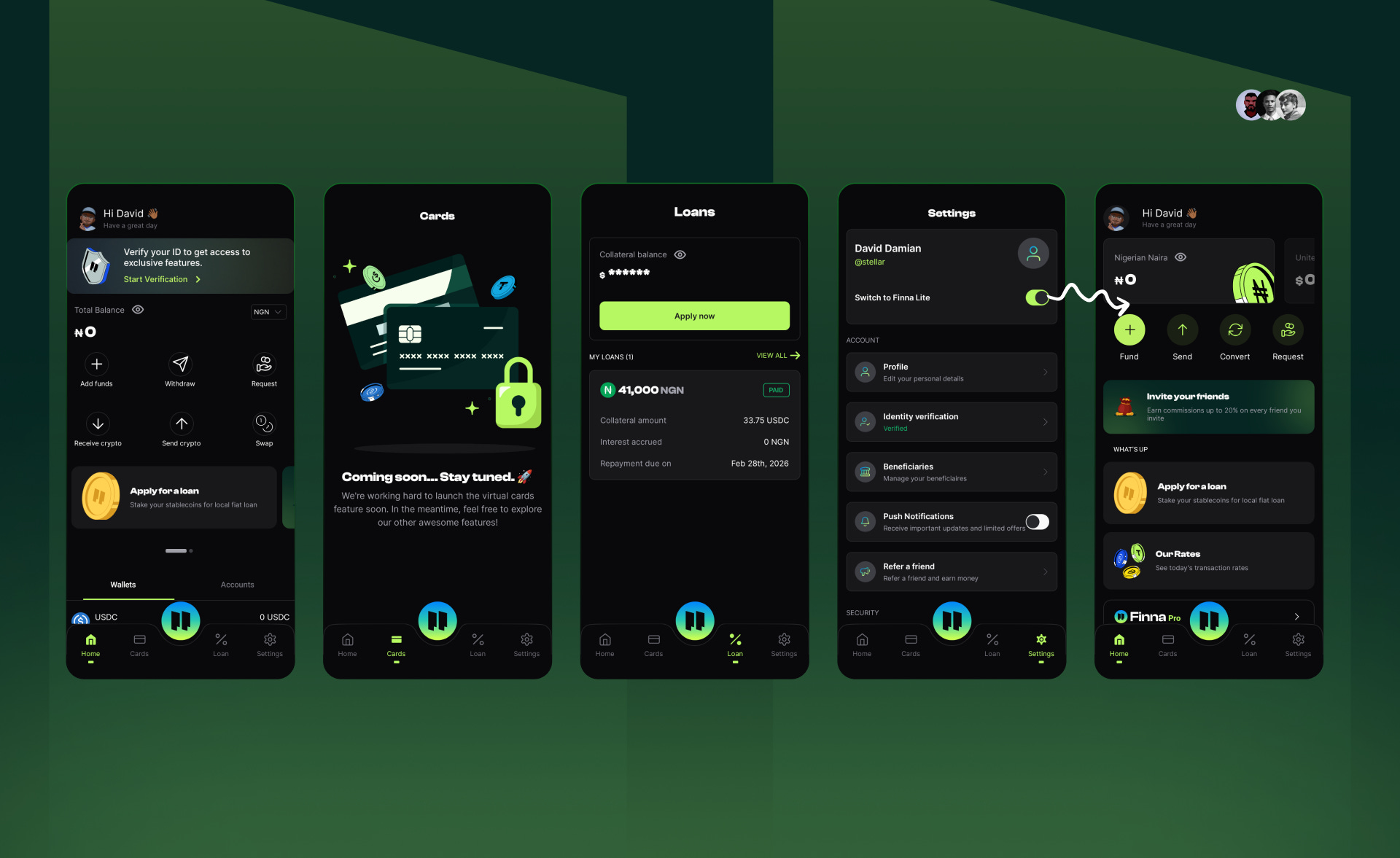

Once you’re on the Home tab, look for the banner that says: ‘Verify your ID to get access to exclusive features.’ Tap ‘Start Verification’ to begin. The process is straightforward. First, verify your phone number, then follow the prompts to link your BVN and NIN and set up Two-Factor Authentication (2FA). These quick steps ensure your account is fully secured and ready for global transactions.

Step 5: Navigating the Interface

The Finna app features four core navigation tabs that structure the user experience:

Home: This serves as your central command center for essential financial actions. From a unified interface, you can add funds, swap assets, withdraw, and send, receive, or request payments. To give you full control over how you view your wealth, the Home tab lets you toggle your primary balance display between Naira and USD at any time. You can also clearly separate digital assets from cash by switching between the “Wallets” view for stablecoins and the “Accounts” view for fiat holdings.

Card (coming soon): Moving over to the card tab, Finna is preparing to bridge the gap between crypto and commerce even further with a virtual card feature that is coming soon, which will allow users to spend their balances directly at online checkouts.

Loan: The is where the true utility of the platform comes to life, allowing you to access instant liquidity by borrowing Naira against your stablecoin holdings.

Settings: Finally, the settings tab offers a secure space to manage your profile details, add and manage beneficiaries, customize security preferences, update your unique Finna username, switch to Finna Lite if you’re not a crypto power user, and access support articles, tutorials, and FAQs to ensure your experience remains seamless.

4.1 Securing a Stablecoin-Backed loan On Finna

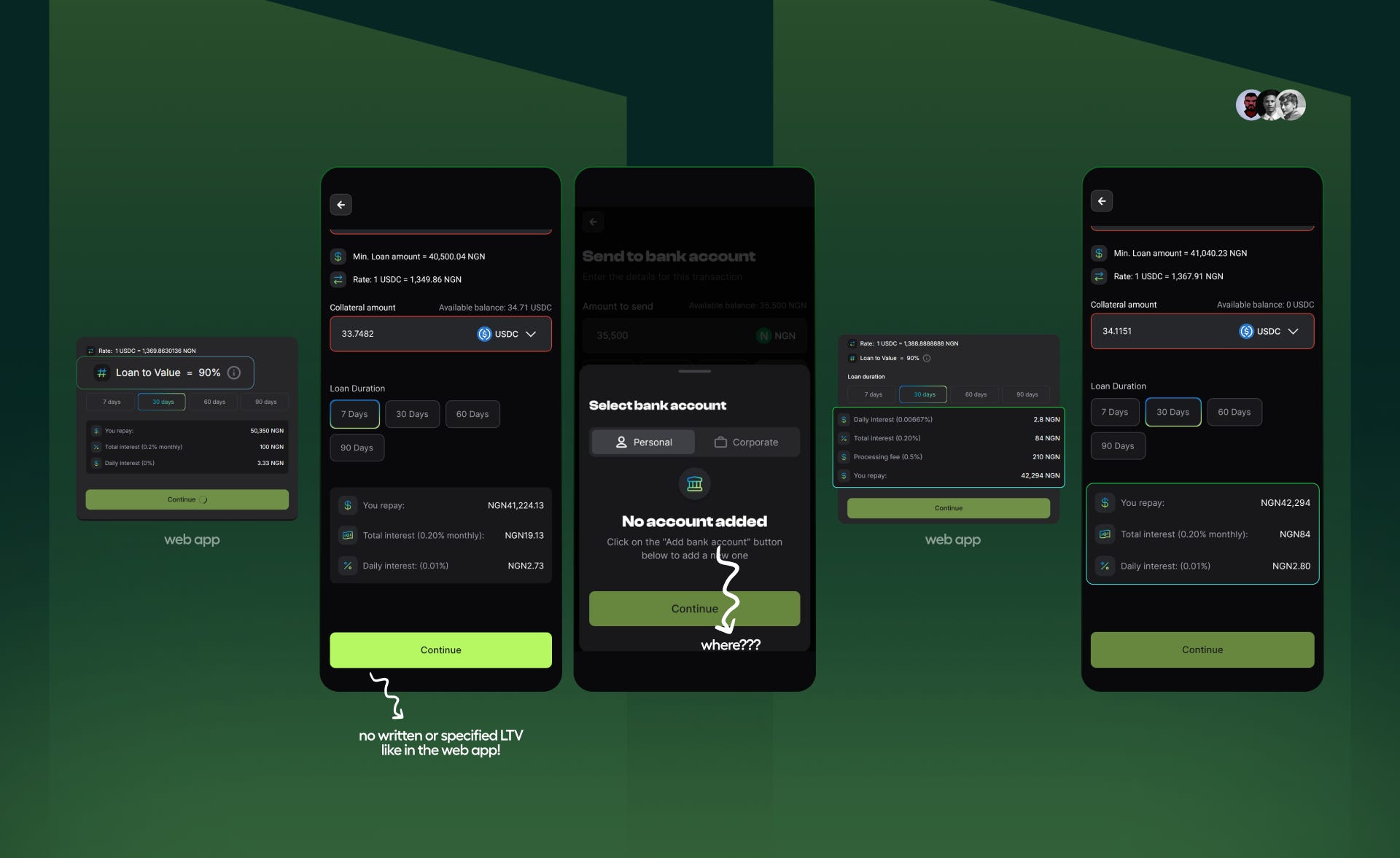

Before you get started, here are a few key parameters to keep in mind regarding the loan feature:

Minimum Threshold: The minimum amount you can borrow is ₦40,500 (at the time of writing).

Collateral Requirements: You must maintain a minimum collateral of ₦45,000 (approximately 33.7 USDC/USDT, at the time of writing).

Interest Rates: Loans carry a competitive 0.20% monthly interest rate, which accrues daily at exactly 0.00667%.

Processing Fee: Please note there is a one-time loan processing fee of 0.5% applied at the start.

Loan-to-Value (LTV): Finna utilizes a 90% LTV ratio, allowing you to unlock maximum liquidity from your assets.

A Note on The Loan-to-Value (LTV) Ratio On Finna

The LTV determines how much cash you can receive relative to the value of the collateral you provide. At a 90% LTV, the formula is:

Loan Amount = Collateral Value x 0.90 (90% = 90 ÷ 100 = 0.90)

What this translate to is that if you have ₦45,000 worth of USDC and you want to take a loan at a 90% LTV, the math looks like this:

45,000 x 0.90 = 40,500

This explains exactly why the minimums are set where they are. To get the minimum loan of ₦40,500, you are required to provide the mathematical equivalent in collateral, which is ₦45,000.

Why This Matters For You

While a 90% LTV is traditionally considered high-risk in the crypto world, where assets like Bitcoin or Solana can drop 10% in a single hour, the math changes when you use stablecoins. On other platforms, such a drop would trigger a “liquidation threshold,” causing the system to automatically sell your collateral to cover the debt.

With Finna, because USDC is pegged to the US Dollar, your collateral value remains stable in dollar terms. The only “risk” is the fluctuation of the USDC/Naira exchange rate. For example, if the Naira strengthens significantly, moving from ₦1,500/$1 to ₦1,000/$1, your USDC becomes worth less in Naira terms, which technically pushes your LTV higher.

Pro-Tip: To sleep better at night, always maintain a buffer. Even though Finna allows up to 90%, borrowing at 70–80% LTV gives you peace of mind and plenty of time to react if the exchange rate shifts.

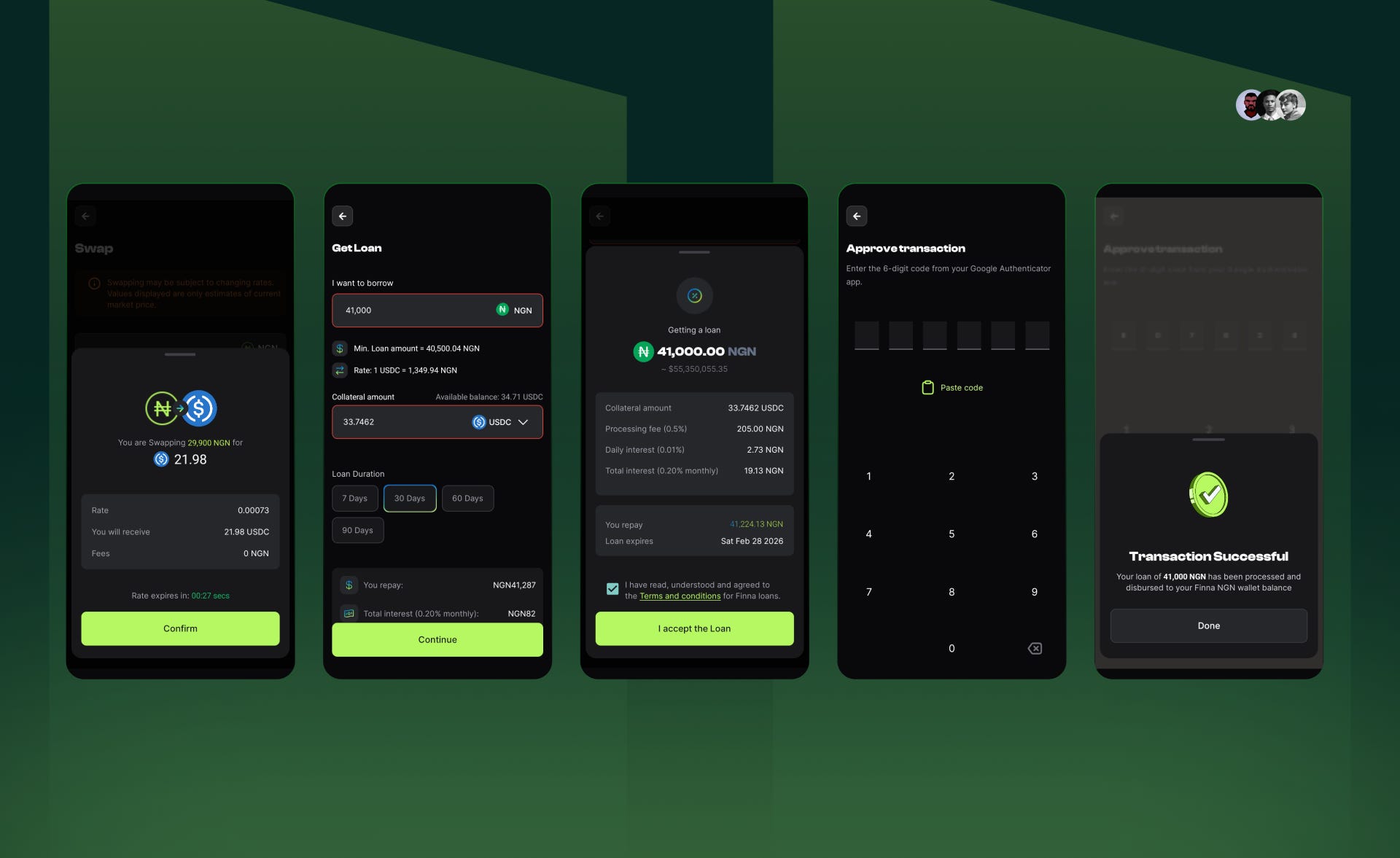

How to Execute

To secure a loan, first top up your USDC/USDT balance to at least ₦45,000. You can do this by using the ‘Receive’ option to deposit Solana-based stablecoins or by using the ‘Deposit’ button to add Naira, which you can then instantly swap for USDC/USDT with zero fees.

Next, head over to the Loan tab to confirm your collateral meets the minimum requirement. If it does, click ‘Apply Now’ and enter the amount of Naira you wish to borrow. The app will automatically calculate your maximum limit based on a 90% LTV of your deposited assets.

You can then specify a loan duration that suits your needs, with options ranging from 7, 30, 60, to 90 days. After reviewing the terms, including the 0.20% monthly interest and the 0.5% processing fee, click ‘I accept the loan’ and authorize the transaction.

The funds will reflect in your Naira wallet balance instantly, and you can track your active loan anytime in the Loan tab.

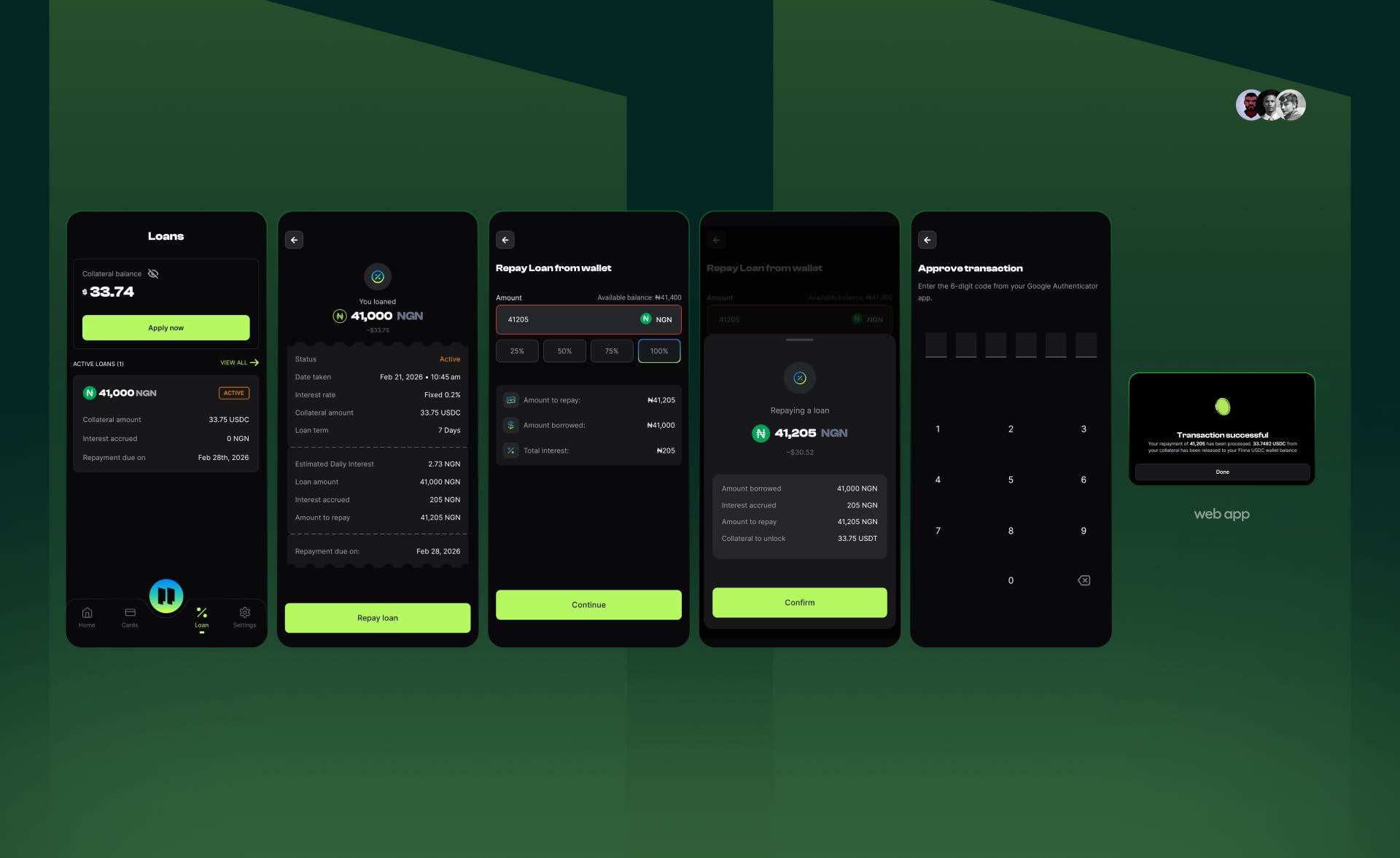

Repaying Your Loan and Reclaiming Your Collateral

To repay your loan, head over to the Loan tab and select your active loan.

Click ‘Repay Loan’ and indicate the amount you wish to settle, you can choose to pay back 25%, 50%, 75%, or 100% of the balance.

Review the final details, including the repayment amount, the original sum borrowed, the total interest accrued, and the specific amount of collateral that will be unlocked.

Once you click ‘Confirm’ and approve the transaction, your USDC/USDT collateral will be instantly released back into your wallet.

4.2 Setting Up Your Finna Tag (username)

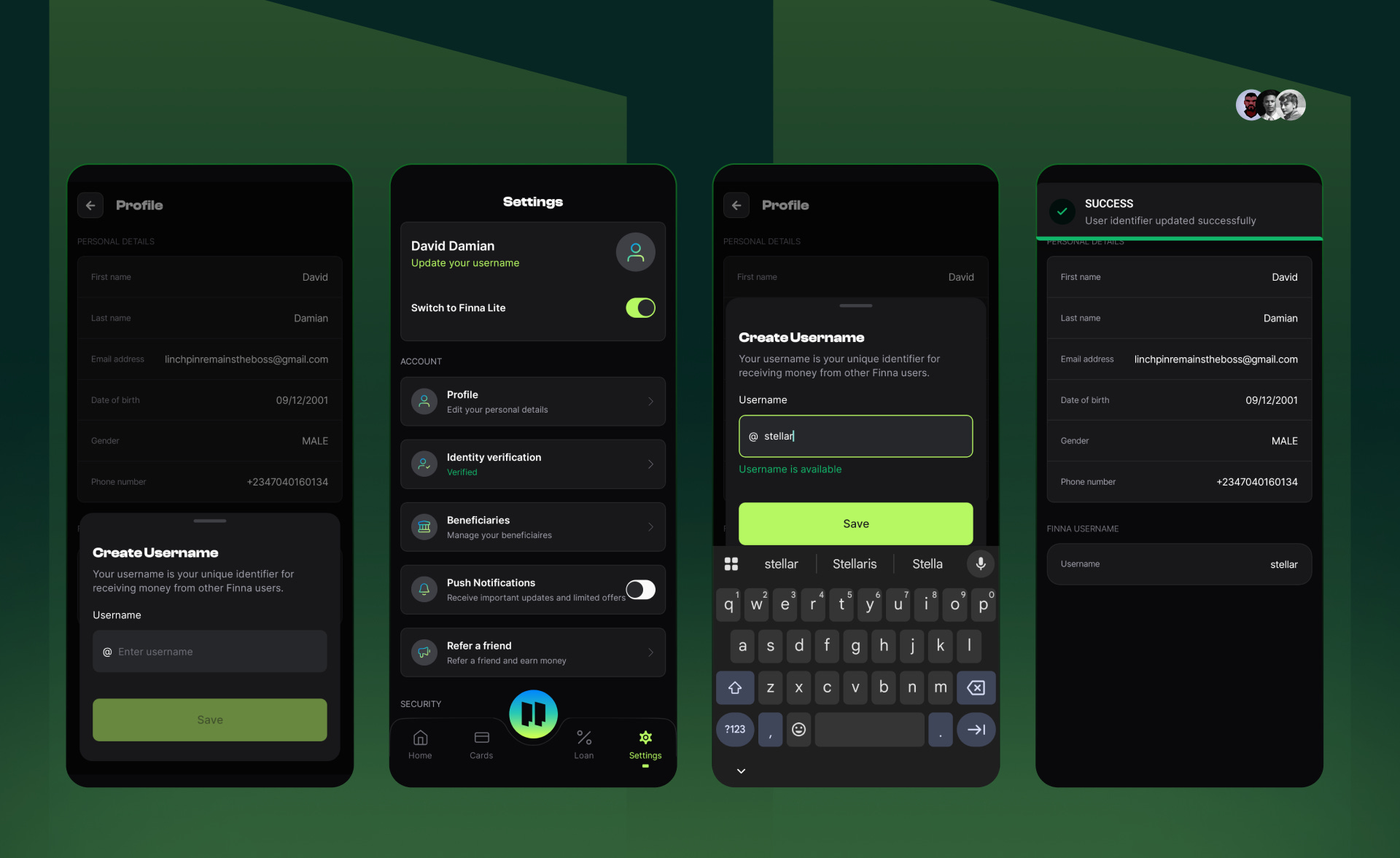

Sending and receiving money on Finna has become an incredibly seamless experience lately, largely thanks to Finna Usernames. This feature removes the headache of copying and pasting long, intimidating wallet addresses and account numbers.

To set yours up, head over to the Settings tab and select “Update your username,” which you’ll find located right under your name. Enter your desired tag, keeping in mind that there is a 10-character limit. Once you hit Save, your unique identity is live.

To send money using a Username, Whether you are sending stablecoins or Naira, the process is instant.

Navigate to the asset you wish to send, click ‘Send,’ and select the option to send to a Finna user via their email or username. Simply enter your friend’s or the receiver’s username and click send.

Best of all? These peer-to-peer transfers come with absolutely zero charges or fees.

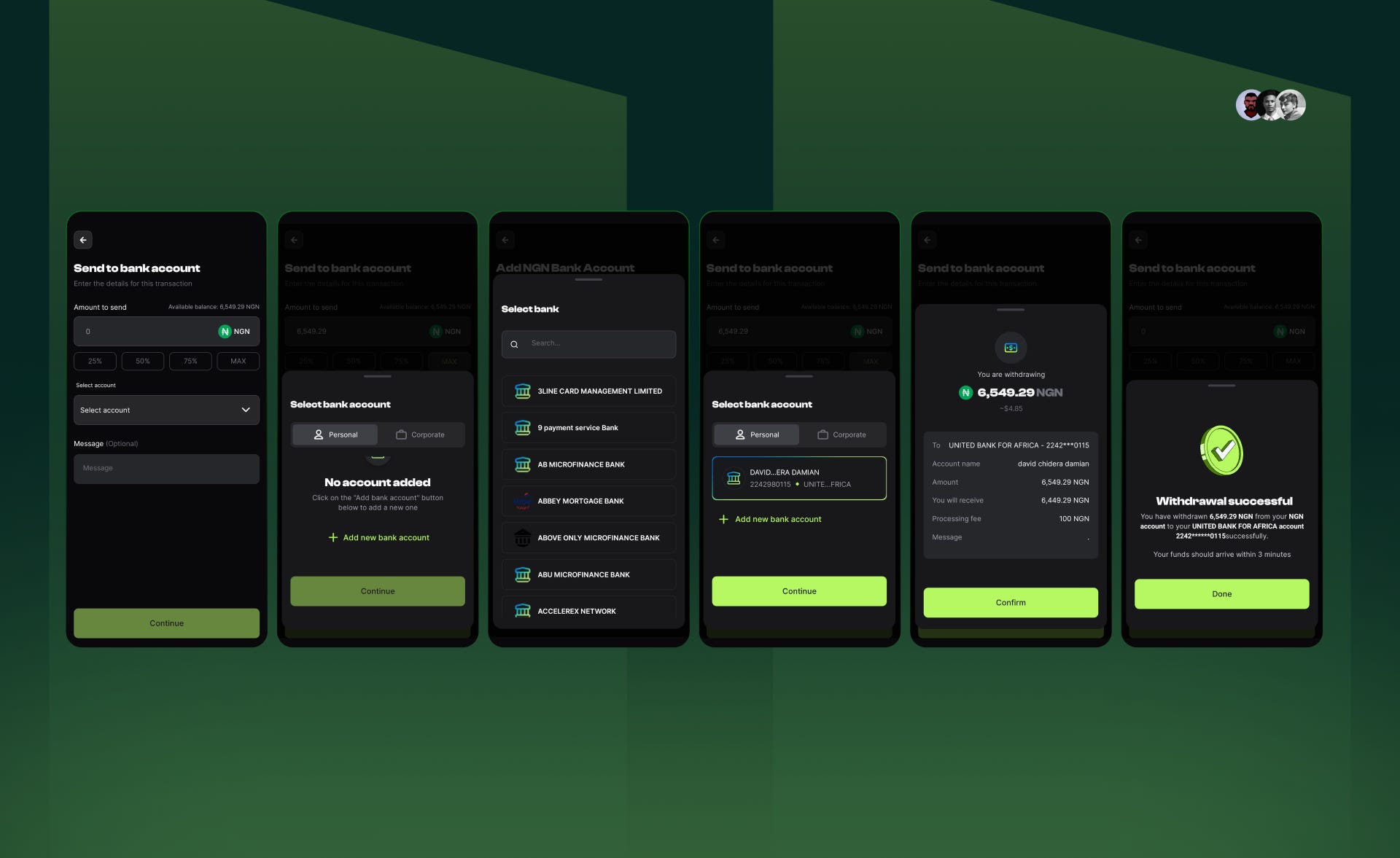

4.3 Off-Ramping: Moving Funds to Your Bank Account

If your funds are currently held in stablecoins like USDC or USDT, the first step is to swap them into Naira within the app. This swap is both instant and completely feeless when using Solana-based stablecoins.

Once your Naira balance is ready, simply click the ‘Send’ or ‘Withdraw’ button and select the Bank Transfer option to proceed.

If you haven’t linked a bank account yet, you can easily do so by selecting whether you are adding a Personal or Corporate account. After entering your bank name and account number, the system will automatically verify and generate the account name for you.

To ensure maximum security and compliance, Finna requires that the name on the bank account matches the name on your verified Finna profile.

With your account successfully linked, enter the amount you wish to withdraw and confirm the details. It is important to note that a flat fee of ₦100 is charged for bank transfers to cover processing and regulatory levies.

After approving the transaction, your funds will be processed and delivered to your bank account, typically in under 3 minutes.

5.0 Feedback & Insight From First-Hand User Experience

This breakdown wouldn’t be complete without an honest look at Finna’s current user interface. During my own testing, I ran into a few points of friction, specifically an incorrect Dollar-to-Naira equivalent displayed on the final loan confirmation screen, and a missing ‘Continue’ button during loan repayment authorization on the mobile app.

I actually had to jump over to the web app to finish my repayment. However, after reaching out directly to the Finna founder, I was assured these specific bugs are being squashed before this article even goes live. The team deserves a shout-out for their swift response and resolution.

That said, there are still a few usability gaps that need to be closed for the experience to be truly world-class:

Direct Off-Ramping: Currently, you have to manually swap stablecoins to Naira before withdrawing to a local bank. To truly close the gap between crypto and fiat, users should be able to off-ramp stablecoins directly to cash in a single click. If the goal is for users to treat USDC like cash, the exit process should be completely frictionless.

LTV Transparency: While the web app clearly displays your 90% Loan-to-Value (LTV) ratio, this crucial detail is currently missing from the mobile interface. Users need to see their LTV at a glance across all platforms to manage their risk effectively.

Real-Time Bugs: On February 22, 2026, a friend testing the app encountered a snag where the “Add Bank Account” button failed to appear on mobile, despite the prompt text. He was able to use the web app to complete the process. Since I didn’t face this issue the day prior, it appears to be a fleeting bug, but it’s one the development team needs to investigate to guarantee friction-free onboarding.

Interest Rate Rounding Errors: There is an active UI discrepancy between platforms regarding interest display. While the total monthly interest is accurately billed at 0.20%, the mobile app visually rounds the daily accrual rate up to 0.01% (which mathematically implies a 0.30% monthly rate). The web interface correctly displays the exact daily rate of 0.00667%. In fintech, users calculate their own risk; front-end rounding inconsistencies like this create immediate mathematical contradictions that can undermine user trust.

Aside from these early-stage constraints, which I am confident will be resolved shortly, the app is genuinely a joy to use. The UI is top-tier. It is sleek, gives off strong “techno vibes,” and feels exactly like the future of Nigerian finance.

6.0 Conclusion

Nigerians are unstable. This statement serves as a double entendre, reflecting both our currency’s volatility and our ironic hesitation to adopt the exact tool designed to bring us stability.

If you’ve read this far, you know that this hesitation isn’t a personal failing. It is the direct result of institutional, social, and infrastructural barriers. While the Federal Government has made strides by lifting the ban on digital currencies and moving toward a clearer regulatory framework, the structural friction of everyday use has remained.

This is exactly where Finna proves its indispensability. It operates as a complete Solana-powered, stablecoin-native ecosystem. By leveraging Solana’s sub-second finality and near-zero costs, Finna strips away the complexities of Web3, making the daily use of USDC and USDT as seamless and intuitive as spending Naira.

Financial stability is no longer a distant ideal locked away in a speculative digital vault. With Finna’s infrastructure, it is a practical reality. The bridge has been built. It is time we cross it and start spending, saving, and sending with the stability we deserve.